With over 35 years of experience serving the shipping and trucking industries, we offer extensive industry expertise. Each month we evaluate multiple resources and provide a recap on current state, trends and what to watch for. See below for this month's industry update.

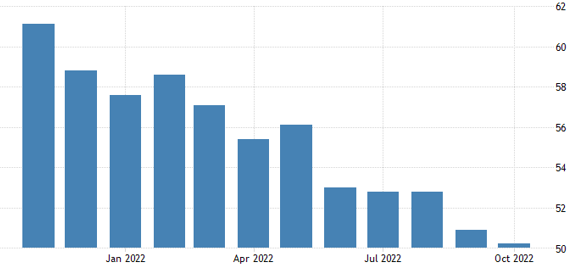

U.S. ISM Manufacturing PMI

- The ISM Manufacturing PMI® for October registered 50.2 percent, 0.7 percentage points below the September reading.

- Economic activity in the manufacturing sector grew in October, with the overall economy achieving a 29th consecutive month of growth. This is the index’s lowest reading since May 2020. Production remained in growth territory while Supplier Deliveries and Backlog of Orders both contracted, all signs that upstream activity is easing. However, bottlenecks are continuing to have impacts further downstream as New Orders remain in contraction and Inventories continue to grow.

Source: Institute for Supply Management

Industry View - October Key Figures (y/y)

- DAT Spot Rates: -12.8% (including fuel)

- Fuel Prices: +44.3%

- ACT Class 8 Preliminary Orders: +96.5%

- ATA NSTA Truck Tonnage: +9.0%

- Cass Freight Expenditures: +20.4%

- Cass Freight Shipments: +6.6%

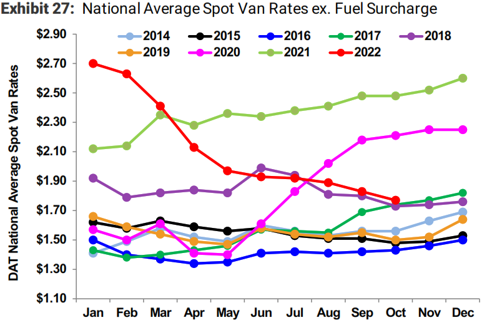

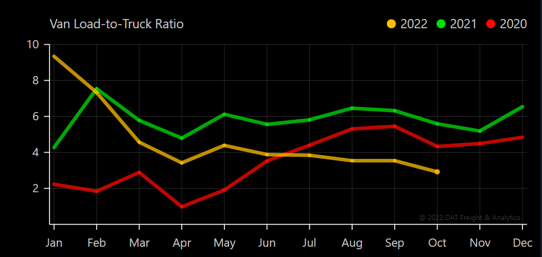

Dry Van

Industry Overview

Van spot rates ex. fuel decreased -28.4% y/y and the van load-to-truck ratio decreased -48.4% y/y.

Market Conditions - Dry Van

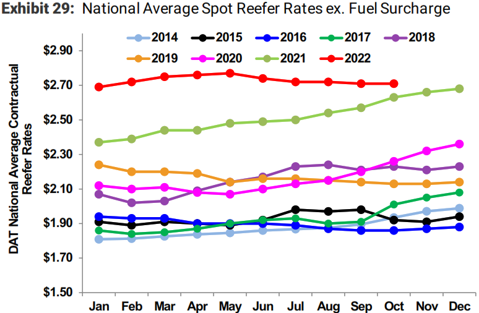

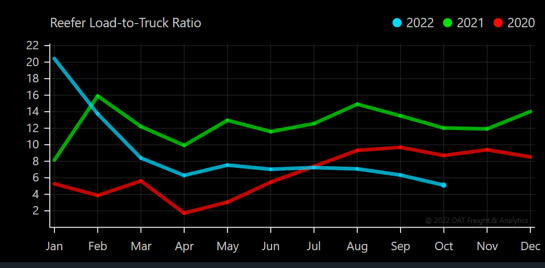

Reefer

Industry Overview

Reefer spot rates ex. fuel decreased -26.8% y/y and the reefer load-to-truck ratio decreased -57.9% y/y.

Market Conditions - Reefer

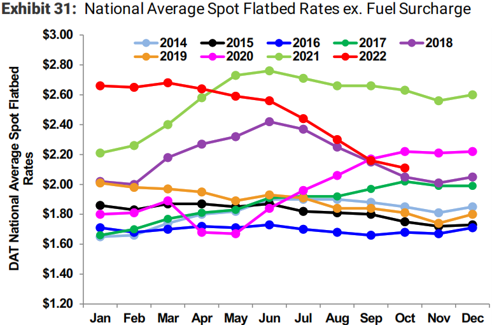

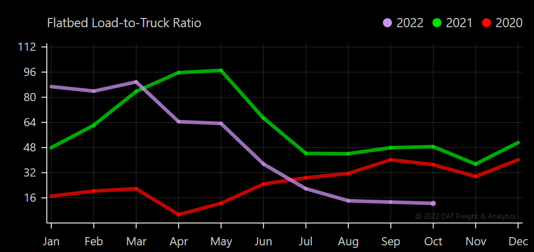

Flatbed

Industry Overview

Flatbed spot rates ex. fuel decreased -20.0% y/y and the flatbed load-to-truck ratio decreased -74.4% y/y.

Market Conditions - Flatbed

DAT Trendlines

November Forecast

- Maritime bookings/imports were down 13% y/y in what is generally considered peak season for ocean freight, indicating that the majority of seasonal inventory is already stateside.

- Consumer demand continues to decline as current inventory levels remain elevated, creating potential for reduced volatility in holiday truckload volume and rate surges.

Keep an eye out for:

- Fuel prices

- Interest rates: The October labor market numbers signal further increases from the Federal Reserve.

- Intermodal rates/capacity: The threat of shutdown due to strikes remains high after two major unions rejected a proposal ahead of the November 19 deadline.

- Consumer spending: Consumer savings levels have hit lows not seen since 2008.

In the News

- Transport Topics: Industry Groups Urge White House to Intercede on Rail Talks

- FreightWaves: Trucking Rate Forecast Suggests Thanksgiving Will Not Be Spot Market Feast

- DC Velocity: Strong Consumer Fundamentals Counter Inflation, Interest Rates in Holiday Forecast

- American Shipper: After Steep September Slide, U.S. Imports Stabilize in October