Back to July 2026 Industry Update

July 2026 Industry Update: Truckload Supply

Main Takeaways

- Tender rejection rates continued to rise in June as carrier utilization remained elevated, signaling ongoing tightness in truckload capacity.

- Strong Class 8 tractor orders reflect growing carrier confidence, though new equipment is unlikely to meaningfully ease capacity constraints in the near term.

Summary

Truckload capacity remained relatively tight in June despite seasonal normalization following disruptions from the CVSA International Roadcheck and the Memorial Day holiday period. Tender rejection rates increased for a second consecutive month, surpassing the 17% threshold, while active truck utilization remained near cycle highs as carriers continue to have ample freight opportunities and greater leverage in load selection. Improving freight fundamentals and strengthening rates have also begun to influence carrier behavior, with Class 8 tractor orders surging as fleets respond to higher equipment utilization and a more favorable operating environment. Although trucking employment was largely stable, the combination of elevated rejection rates, strong equipment demand and high utilization levels suggests available capacity remains constrained relative to freight demand.

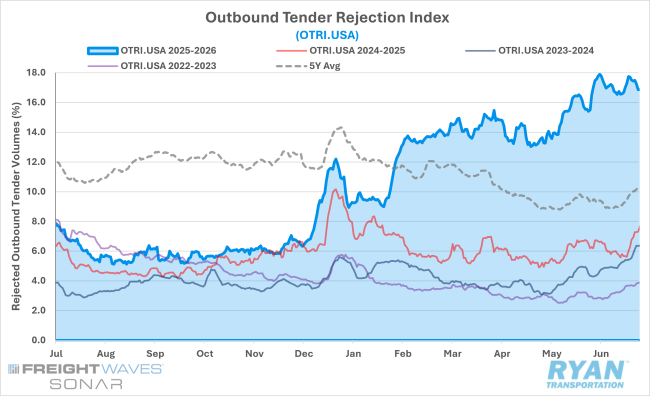

SONAR Outbound Tender Rejection Index (OTRI.USA)

Key Points

- Outbound tender rejections rose further for the second straight month in June, jumping 216 bps MoM to 17.2%.

- Rejection rates remain elevated compared to year-ago levels, with current OTRI levels averaging roughly 10.8% higher YoY than in June 2025.

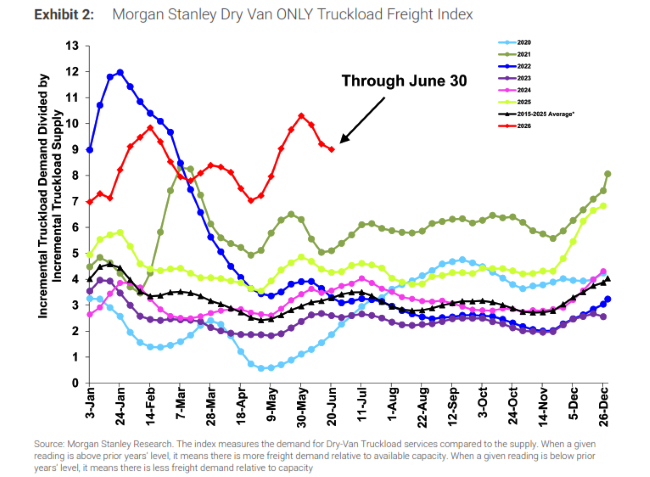

Morgan Stanley Truckload Freight Index

Key Points

- The Morgan Stanley Truckload Freight Index declined sequentially and reverted to underperformance relative to normal seasonality, following a stretch of strong outperformance over the last 3 months, due to weakness in both the supply and demand components.

- Both the reefer and flatbed indices also decreased sequentially in June, with both continuing to underperform typical seasonality.

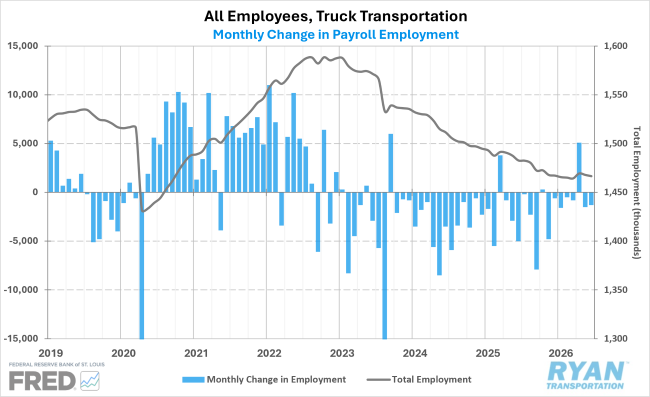

Truck Transportation Payroll Employment

Key Points

- For-hire trucking employment declined by 1,300 payroll jobs on a seasonally adjusted basis in June following substantial upward revisions to earlier preliminary estimates in May and April, according to the latest employment report released by the Bureau of Labor Statistics (BLS).

- Updated BLS figures for April and May resulted in a net increase of 5,100 jobs in April, 200 more than the previous estimate and a net decline of 1,500 jobs in May, down from the previously reported decline of 4,400 payroll jobs.

- More granular data available only through May reflected a decline of 400 jobs in general freight truckload employment while general freight LTL employment increased by 1,000 jobs.

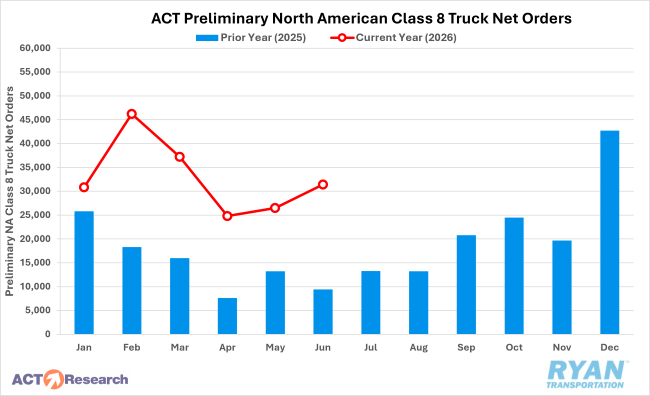

Preliminary North American Class 8 Tractor Net Orders

Key Points

- Preliminary North American Class 8 truck orders remained strong in June, with FTR and ACT Research reporting estimates ranging from 30,500 to 31,400 units, marking an increase of ~15% and 18.5% YoY, respectively.

- On an annual basis, preliminary orders were up between 234% and 241% YoY, as replacement needs, firmer freight rates and limited remaining 2026 build-slot availability continue to drive tractor demand.

- According to FTR, Class 8 orders are up 125% YTD, with the current order season (September-June) registering 36% higher YoY compared to the same time last year, with June’s total coming in 68% above the 10-year average for the month, representing the second largest June net order total since FTR began tracking this metric.

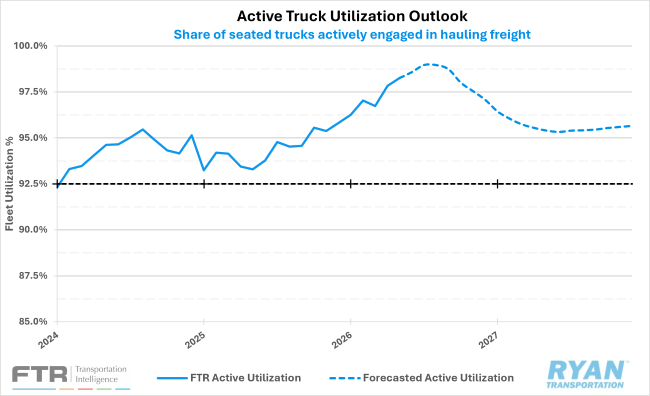

FTR Active Truck Utilization

Key Points

- FTR's active truck utilization outlook was mostly unchanged from the prior forecast in June, with active utilization still expected to peak around 99% in July and August before softening into 2027 to around 96%, remaining well above the 10-year average.

- According to FTR, the continued policy enforcement against foreign truck drivers has created an unprecedented dynamic, making future impacts on capacity levels difficult to assess.

Outlook

Looking ahead, capacity conditions should normalize in line with typical seasonal patterns following the Fourth of July disruptions. Some potential for volatility remains, as targeted enforcement efforts against foreign truck drivers and broader policy uncertainty could contribute to localized capacity constraints. Limited available build slots and potential increases in emissions and trade regulation costs will continue to drive equipment demand through the year, while low driver availability and delayed production times will restrain fleet expansion. However, active utilization is expected to peak in July and August, supporting an environment in which carriers will maintain strong pricing power and tender rejections will remain elevated.