Back to July 2026 Industry Update

July 2026 Industry Update: Truckload Rates

Main Takeaways

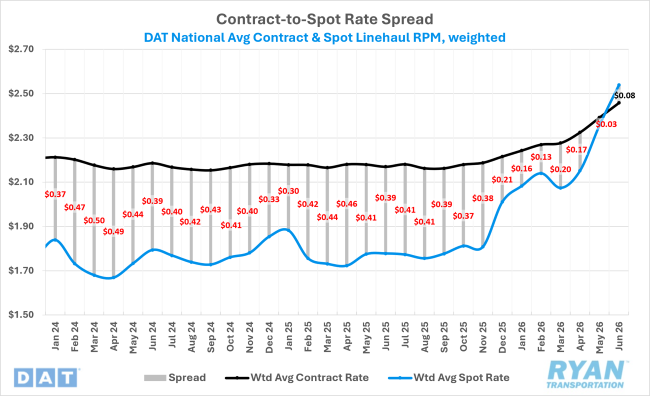

- Spot truckload rates continued to surge in June, pushing market pricing above contract rates for the first time in more than four years.

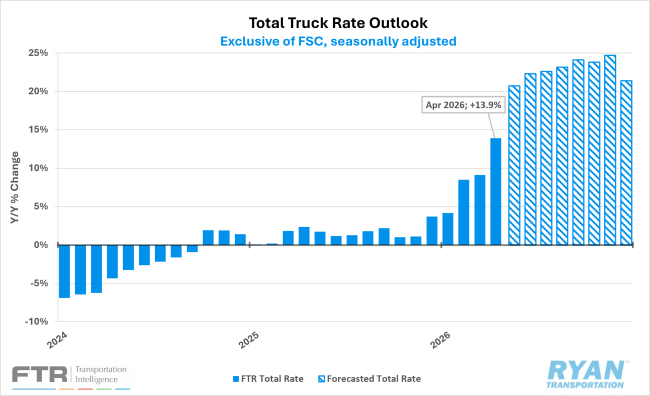

- Tightening capacity conditions and rising carrier utilization are expected to support further increases in contract rates through the remainder of 2026.

Summary

Following record-setting gains during CVSA Roadcheck week, which extended through Memorial Day and into early June, spot rate activity normalized as capacity conditions stabilized. The end-of-quarter volume push and the upcoming holiday weekend resulted in a late-month rally. Tight capacity conditions and elevated utilization in the first and final weeks resulted in total truckload spot rates posting a second consecutive month of double-digit-cent gains, rising above the levels recorded in the same month during the bull market of 2021. The rapid acceleration in spot rates resulted in the inversion of the contract premium for the first time in four years, adding further upward pressure on contract pricing as carriers increasingly seek out higher-priced spot opportunities over contractual commitments.

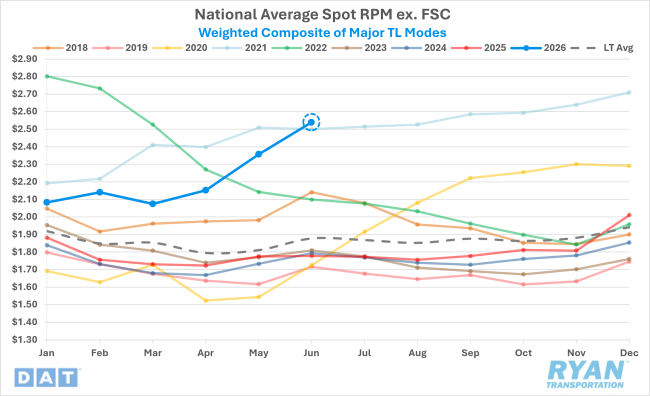

DAT National Average Spot Rates excl. FSC, Weighted Composite Index

Key Points

- Total average truckload spot linehaul rates continued to increase sharply in June, rising by 7.7% MoM ($0.18) after surging by $0.20 MoM in May.

- Compared to June 2025, total truckload spot rates excluding fuel are 42.8% ($0.76) higher YoY and are 34.8% ($0.66) above the long-term average.

DAT National Average RPM Contract vs. Spot

Key Points

- Initially reported total truckload contract linehaul rates increased 2.8% MoM ($0.07) and were up 13.3% YoY ($0.29).

- After narrowing sharply over the last two months, the contract-to-spot spread inverted in June, with initially reported contract rates now trending at a 3.2% ($0.08) discount relative to spot rates for the first time since January 2022.

FTR Total Truck Rate & Outlook

Key Points

- After rising by 4 points from the prior outlook in May, FTR’s 2026 forecast for total truckload rates rose by nearly as much in the latest update, with total truckload rates expected to be +18.2% YoY, excluding fuel, up from the previously projected +14.4% YoY growth.

- Spot rate growth continues to drive strong upward revisions, with total truckload spot rates projected to grow +35.3% YoY, up from +28% in the prior outlook, while the total truckload contract rate forecast was revised up to +10.1% YoY growth from +7.9% previously.

- By equipment type, the outlook for flatbed rate growth remains the strongest at +19.3% YoY (up from +15.2% previously), followed by forecasted dry van rate growth of +18.3% YoY (+14.6% previously) and reefer rate growth of +17.9% YoY (+14.9% previously).

DAT Fuel Trends

Key Points

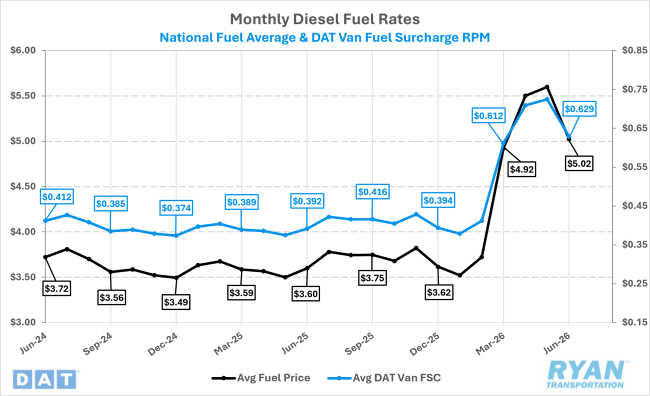

- The national average monthly diesel price declined sharply by nearly $0.58 MoM in June, dropping from $5.60 in May to $5.02, but remains roughly $1.43 above June 2025 levels.

- In its latest Short Term Energy Outlook (STEO), the Energy Information Administration expects retail diesel prices to fall by just over 4% in the second half of the year compared to the first half and to continue declining steadily throughout 2027, registering roughly 13% lower YoY than in 2026.

Outlook

The rate environment is expected to remain favorable for carriers through the balance of the summer as active capacity remains constrained and freight networks continue to experience elevated tender rejection activity. While seasonal demand patterns typically support a period of rate stabilization following the Independence Day holiday, potential additional capacity disruptions from upcoming CVSA enforcement events and continued pressure on carrier utilization could create localized pricing volatility. The recent inversion of the contract-to-spot spread is also likely to increase contract renegotiation activity, placing upward pressure on contractual transportation rates through the second half of the year.