Back to July 2026 Industry Update

July 2026 Industry Update: Truckload Demand

Main Takeaways

- Freight demand remained stable in June, supported by recovering contract volumes, resilient import activity and continued strength in consumer spending.

- Growing signs of inventory replenishment and import front-loading could support freight volumes later this year, though intermodal competition may limit truckload market upside.

Summary

Truckload demand remained stable in June, with freight volumes benefiting from a post-Memorial Day rebound early in the month and a seasonal end-of-quarter shipping push ahead of the Independence Day holiday. Contract freight volumes recovered from May's decline, while spot market activity remained unchanged sequentially and continued to outperform year-ago levels for the fifteenth consecutive month. Broader freight indicators also pointed to gradually improving demand fundamentals, including stronger inventory growth, resilient import activity, and freight shipment trends that are nearing positive year-over-year territory. While some inventory replenishment and import activity may reflect precautionary ordering ahead of potential tariff changes, underlying demand remains supported by healthy consumer spending and steady manufacturing activity.

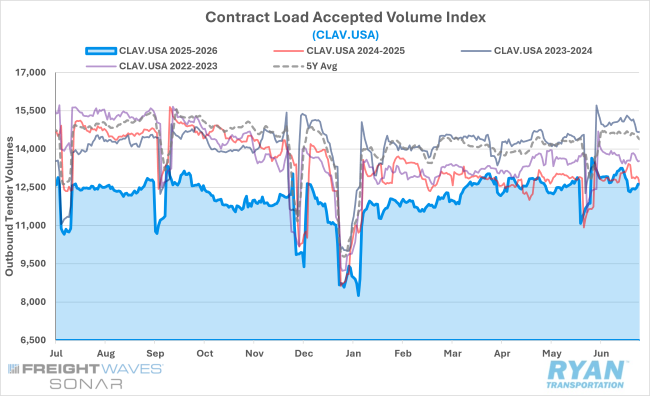

SONAR Contract Load Accepted Volumes Index (CLAV.USA)

Key Points

- Following a slight dip in May after a four-month growth streak to start the year, tender volumes accepted under contract rebounded in June, rising by 4.7% MoM. Removing post-Memorial Day distortion, accepted tender volumes were up just 2.9% MoM.

- After turning positive for the first time in over three years in April, annual comparisons remained negative for the second straight month, though just barely in June, registering 0.1% lower YoY compared to June 2025 levels.

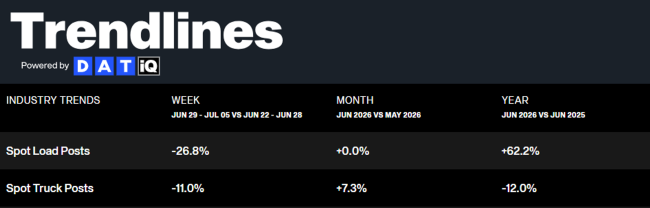

DAT Trendlines

Key Points

- Spot market activity was unchanged from May in June but remained well above year-ago levels for the 15th consecutive month.

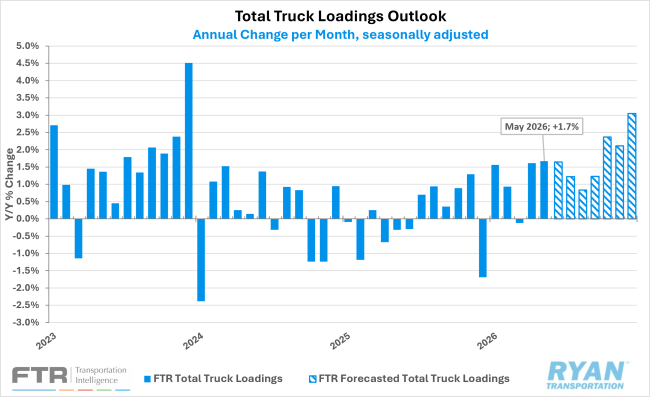

FTR Total Truck Loadings Outlook

Key Points

- In its latest forecast, FTR revised its total truck loadings for 2026 up slightly to +1.5% YoY growth from the previously reported +1.3% growth, driven by continued improvement in bulk aggregate loadings.

- The forecast across all equipment types was mixed, as flatbed and reefer loadings both rose slightly by just 10 bps to +3.7% YoY and +1.9% growth, respectively, while softer automotive loadings and a slightly more negative outlook for food resulted in downward revisions in the dry van loading outlook to +1.3% YoY, down from the previously reported +1.7% growth.

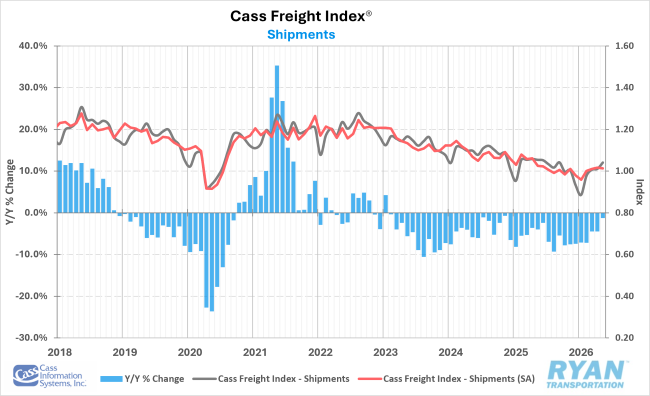

Cass Freight Index Shipments Forecast – May 2026

Key Points

- The shipments component of the Cass Freight Index® rose 3.0% MoM in May, bringing annual comparisons to their slimmest negative margin in 18 months at 1.2% below YoY.

- Seasonally adjusted, shipments in May were down just 0.3% MoM, setting up a 1.8% YoY increase in the second half of 2026 with YoY comps expected to turn positive in July based on that trend.

- According to the Cass report, the normal seasonal trend would put the shipments component down roughly 1% YoY in June.

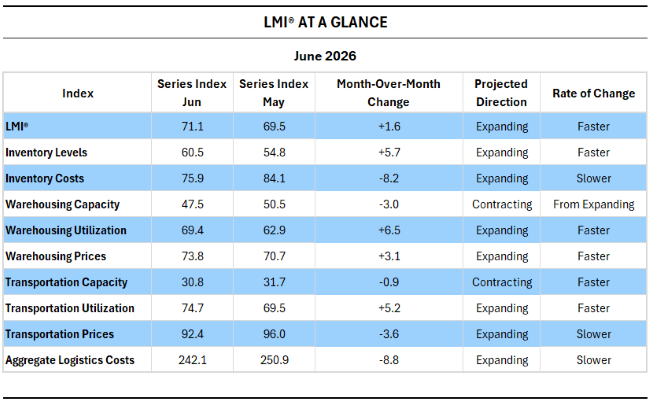

LMI® AT A GLANCE

Key Points

- The LMI® read in at 71.1 in June, up (+1.6) from May’s reading of 69.5 and marking the first time the overall index has read in above 70.0 — considered to be a significant rate of expansion — since March 2022, when the index hit 76.2.

- The upward push in June was largely driven by a much faster rate of expansion in Inventory Levels (+5.7 to 60.5), which led to subsequent increases in both Warehousing Utilization and Warehousing Prices, as well as continued strength across the three transportation metrics.

- Per the LMI® report, the Inventory Level expansion is a reversal from what has been observed for much of 2026, as the push from retailers likely represents either increased confidence to bring forward goods for the second half of the year due to ongoing strength in consumer spending, or the potential for an increase in tariffs later in July resulting in a pull-forward ahead of traditional peak season.

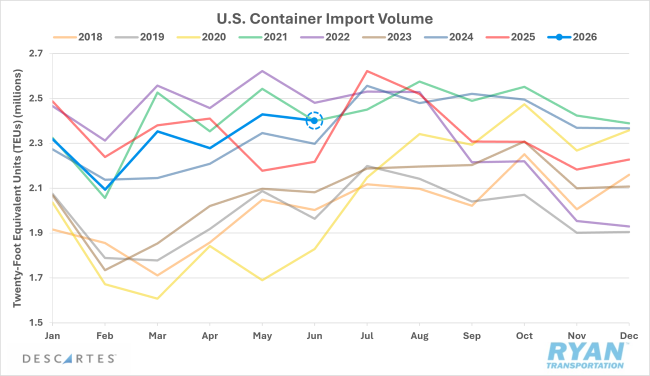

Descartes U.S. Container Import Volumes

Key Points

- U.S. containerized imports softened slightly in June from May but were mostly stable, registering 1.2% lower MoM but up 8.2% YoY compared to June 2025.

- June’s decline was reflective of typical seasonal easing that follows May’s import growth, though YTD imports are essentially flat compared to the same month last year, registering just 0.3% lower YoY but 19.5% higher compared to the same time frame in 2019.

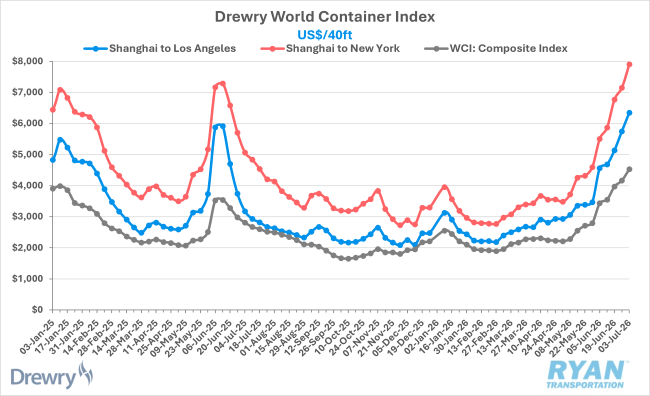

Drewry World Container Index

Key Points

- Early peak-season demand, driven by geopolitical uncertainty and cargo frontloading to get ahead of general rate increases and peak-season surcharges expected to go into effect in July, caused global container rates to climb in June, with the WCI rising 32% MoM and registering 61.1% higher YoY, its highest level since September 2024.

- Transpacific routes were the primary drivers of gains in global container rates, with Shanghai to Los Angeles rising 39.1% MoM and 99.7% YoY in the final week of June, while Shanghai to New York rose 43.5% MoM and was up 55.1% YoY compared to the same week in 2025.

Outlook

Looking ahead, truckload demand is expected to follow normal seasonal patterns and moderate slightly following the Fourth of July holiday before strengthening later in the third quarter as back-to-school and peak shipping season activity ramps up. Unlike previous freight upcycles that were driven by a sudden demand shock, current demand growth remains more gradual, supported by improving manufacturing output, stable consumer spending, and modest inventory rebuilding. Recent increases in inventory levels, elevated import volumes, and rising transpacific container rates suggest shippers may once again pull freight forward in anticipation of future trade policy changes. However, high inventory carrying costs and the significant cost advantage of intermodal transportation could limit the extent to which additional import-driven freight translates into growth in truckload volume.