Back to July 2026 Industry Update

July 2026 Industry Update: U.S. Economy

Main Takeaways

- U.S. manufacturing activity expanded for a sixth consecutive month in June, supported by healthy order activity, lean customer inventories and continued strength in domestic demand despite moderating growth rates.

- Consumer spending remained an economic bright spot, offsetting ongoing weakness in housing, softer export demand and growing uncertainty surrounding trade and labor market conditions.

Summary

U.S. economic conditions remained generally supportive in June, led by continued expansion in domestic manufacturing activity and resilient consumer spending. Manufacturing growth extended for a sixth consecutive month, though at a slower rate than in May, supported by expanding inventories, healthy order backlogs and customer inventory levels that remain relatively lean. Consumer spending accelerated to its strongest year-over-year growth rate in more than four years as spending and wage gaps between income cohorts narrowed further. Offsetting some of this strength, housing activity weakened considerably, labor market growth continued to slow and inflationary pressures remained persistent.

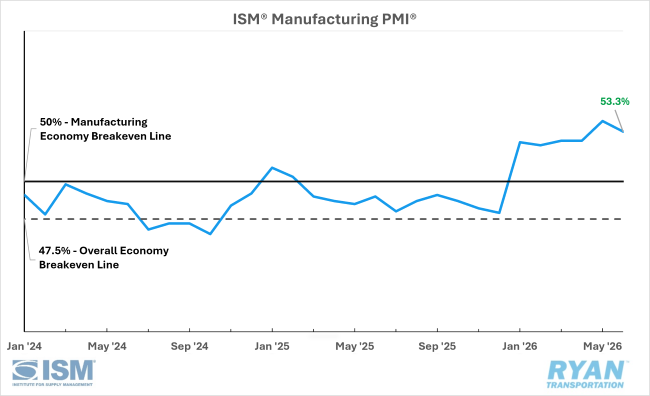

United States ISM Manufacturing PMI

Key Points

- Domestic manufacturing activity continued to expand for the sixth consecutive month in June, at a faster rate than in May, with the ISM® Manufacturing PMI® reading at 53.3%, a 0.7 percentage-point drop from the 54.0% registered last month.

- All but one (Petroleum & Coal Products) of the six largest manufacturing industries expanded in June, in the following order: Computer & Electronic Products; Machinery; Transportation Equipment; Chemical Products; and Food, Beverage & Tobacco Products.

- In the manufacturing economy, 5% of the sector’s gross domestic product (GDP) contracted in June, up from 2% in May, while 3% was in strong contraction, compared to 2% last month.

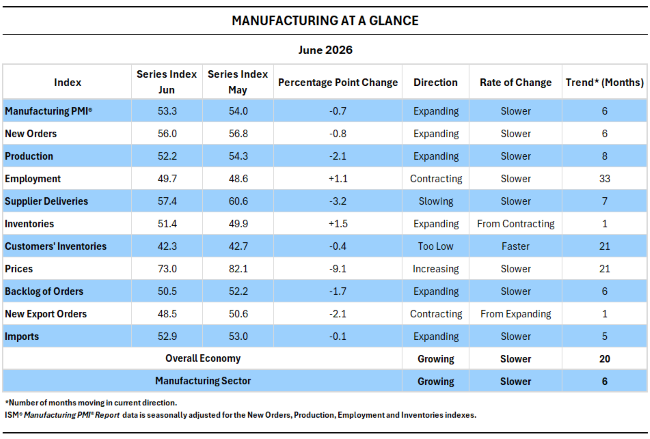

Manufacturing at a Glance

Key Points

- Of the five subindexes that directly factor into the Manufacturing PMI®, two (Employment and Inventories) registered improvement in June from May, with the latter moving into expansion territory, while three (New Orders, Production and Supplier Deliveries) remained in expansion territory in June but at a slower rate compared to last month.

- Overall demand indicators were positive despite slower growth in the New Orders and Backlog of Orders indexes, as Customers’ Inventories remain in “too low” territory and panelists' comments registered a 2.7-to-1 ratio of positive to negative.

- Output was also largely positive, as the Production index recorded an eighth consecutive month of expansion, while Employment increased by 1.1 percentage points to a mild contraction. According to survey responses, 64% of panelists’ companies are hiring — a near reversal from the start of the year when 66% of companies were managing staffing levels in the January report.

- Inputs were mixed, with the Supplier Deliveries index dropping 3.2 percentage points and Inventories moving into expansion, while Prices declined 9.1 percentage points to 73% in June, down from 82.1% in May.

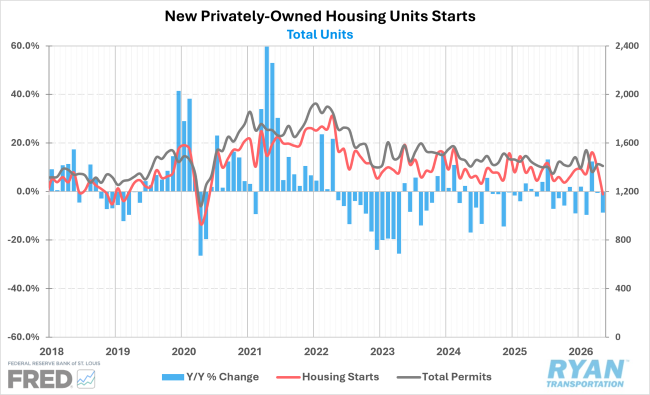

New Residential Construction

Key Points

- Seasonally adjusted housing starts fell 15.4% MoM, the largest drop in more than two years, and were down 8.7% YoY in May to an annualized rate of 1.18 million units, the lowest level since February 2019, except for the two pandemic lockdown months of April and May 2020.

- Single-family home starts were down 1.9% MoM and registered 6.7% lower YoY, while starts for multi-family dwellings of five or more units plunged 41.6% MoM and were down 12.3% YoY.

- Permits authorized for future construction were far more stable, however, with total build permits declining by just 0.7% MoM and down 0.2% YoY. Permits for multi-family homes drove the weakness, declining 3.5% MoM but remaining up 3.0% YoY, while single-family permits increased 1.2% MoM but are still down 1.1% YoY.

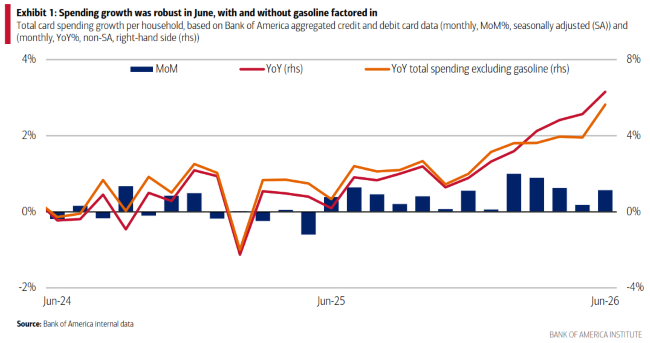

Bank of America Consumer Checkpoint, Total Card Spending

Key Points

- Consumer spending remained strong in June, rising 0.6% MoM and increasing 6.3% YoY, the strongest rate of growth since April 2022.

- With total gasoline prices easing in June, total card spending excluding gas surged 5.6% YoY, also the strongest growth rate since April 2022 and up from 3.9% YoY in May, indicating most of June’s spending growth was discretionary.

- Spending gaps between income cohorts continued to narrow in June, with lower-income household spending registering the largest boost, followed by middle-income households, rising to 4.8% YoY from 4.1% YoY and 4.3% YoY, respectively, in May. Meanwhile, higher-income household spending rose more modestly to 5.8% YoY in June from 5.5% YoY in May.

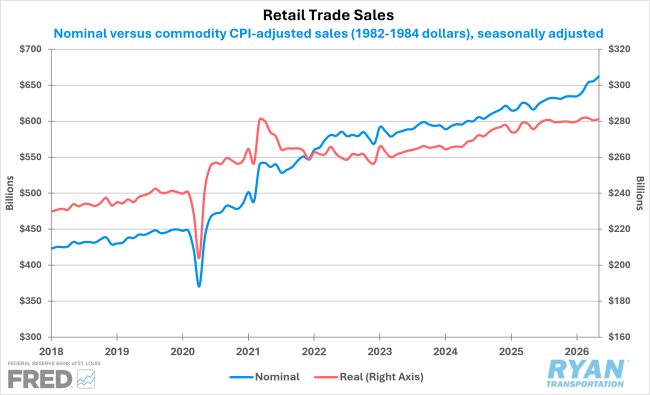

Advanced Retail Trade Sales

Key Points

- Retail and food service sales increased 0.9% MoM and were up 6.9% YoY in May.

- Excluding food service sales from restaurants and bars, retail trade sales increased 1.0% MoM and were up 7.5% YoY, though much of this remains driven by inflation, largely due to gas prices. When adjusted by the Consumer Price Index for commodities, real retail trade sales were up just 0.3% MoM and 2.1% YoY.

Outlook

Looking ahead, the economic outlook remains constructive but increasingly dependent on domestic demand. Consumer spending and ongoing manufacturing expansion should continue to support freight activity through the second half of the year, particularly as retailers prepare for the back-to-school and holiday shopping seasons. However, uncertainty surrounding trade policy, elevated borrowing costs, slowing job growth and continued weakness in residential construction may temper overall economic momentum.