Back to May 2026 Industry Update

May 2026 Industry Update: Truckload Supply

Main Takeaways

- Tender rejections weakened from March but are still trending at their highest levels in over four years.

- The for-hire carrier population registered its largest increase since September 2022 as new entrants rose while revocations fell.

Summary

After early-month pressures tied to end-of-quarter shipping activity and the Easter holiday subsided, outbound tender rejections eased in April in line with seasonal expectations, declining from March levels but remaining well above prior-year averages. Signs of incremental capacity returning to the market were reflected in a sharp increase in the for-hire carrier population and a notable rise in truckload payroll employment. Meanwhile, equipment orders moderated from March levels largely due to normal seasonal patterns rather than weakening demand, with overall order activity remaining significantly above 2025 levels.

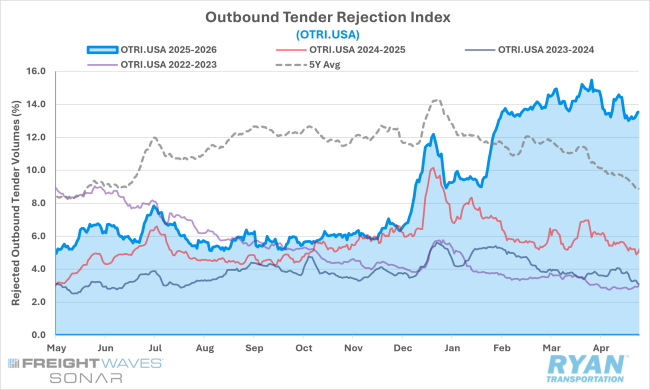

SONAR Outbound Tender Rejection Index (OTRI.USA)

Key Points

- After seven consecutive months of increases, outbound tender rejections declined approximately 50 basis points MoM in April to 13.9%.

- Despite seasonal easing, rejection rates remained elevated at 8.3% above year‑ago levels and 10.3% higher on a two‑year stacked basis.

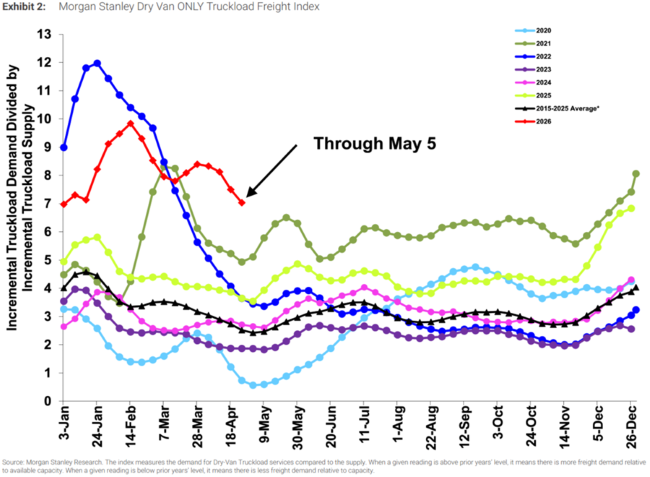

Morgan Stanley Truckload Freight Index

Key Points

- The Morgan Stanley Truckload Freight Index continued to outperform seasonal norms in April, supported by strength in both supply and demand components.

- Reefer and flatbed indices declined sequentially, though reefer conditions strengthened later in the month while flatbed performance remained broadly in line with typical seasonality.

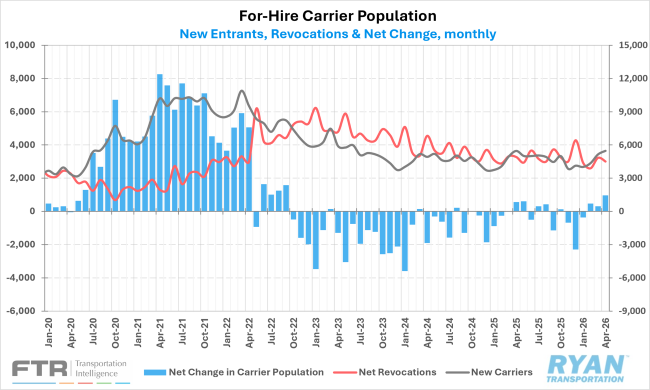

New Authorities, Net Revocations & Net Change in For-Hire Carrier Population

Key Points

- FMCSA authorized 5,479 new for‑hire carriers in April, the largest monthly increase since June 2022, and up more than 320 carriers from March.

- Net revocations totaled 4,512 carriers, resulting in a net increase of 967 carriers — the largest monthly gain since September 2022 — and marking a third consecutive month of growth.

- The active for‑hire carrier population remains more than 34% above pre‑pandemic levels, representing over 86,000 additional carriers.

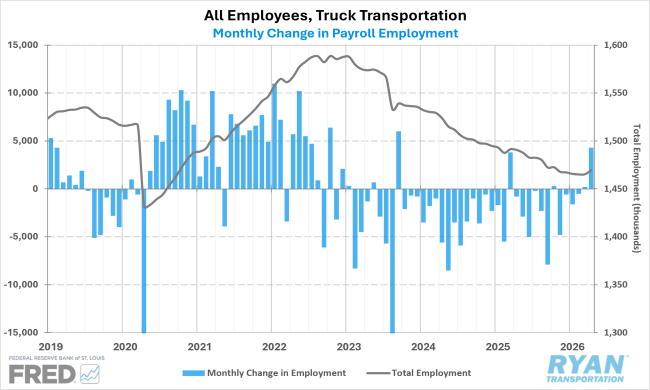

Truck Transportation Payroll Employment

Key Points

- Truck transportation employment increased by 4,300 jobs in April, the largest monthly gain since September 2023, following upward revisions to February and March payroll data.

- Employment levels remain 3.1% below February 2020 levels, indicating continued structural tightness in the labor market.

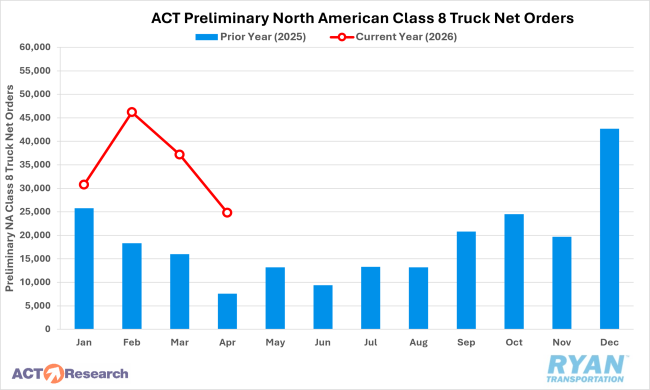

Preliminary North American Class 8 Tractor Net Orders

Key Points

- Preliminary Class 8 orders declined approximately 33% MoM in April to a range of 24,800 – 25,500 units, reflecting typical seasonal pullbacks after March’s unusually strong order volume.

- Despite sequential declines, orders remained elevated by roughly 200% YoY compared to April 2025.

- Order activity is expected to soften until 2027 order books open in September, as 2026 production slots fill earlier than usual.

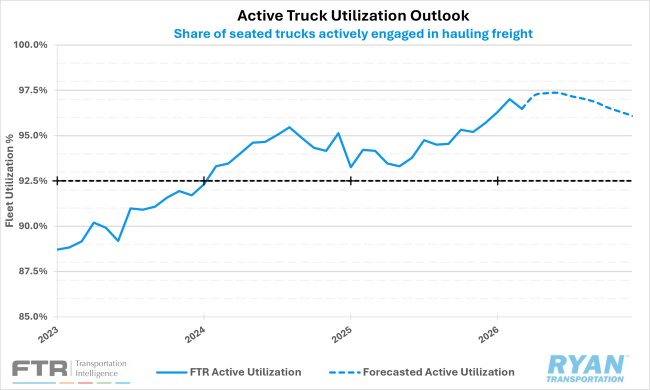

FTR Active Truck Utilization

Key Points

- FTR revised its active utilization outlook slightly lower but continues to project utilization peaking just above 97% by mid‑year before gradually easing into 2027.

- Despite recent rate strength and market disruptions, limited freight volume growth is expected to cap utilization gains, suggesting spot rates are unlikely to accelerate significantly but are also unlikely to deteriorate meaningfully.

Outlook

Capacity tightness is expected to increase markedly in the near term with the onset of CVSA International Roadcheck in mid-May, followed immediately by the lead-up to Memorial Day weekend. In addition to the standard maintenance and safety inspections associated with DOT “Blitz Week,” stricter enforcement of English Language Proficiency and non-domiciled CDL requirements is likely to result in more drivers coming off the road, both voluntarily and involuntarily. However, the sustainability of these tighter capacity conditions remains uncertain, as improving freight demand and stronger rate environments may increasingly incentivize previously sidelined carriers to re-enter the market, as reflected by recent gains in for-hire carrier authorities and rising employment levels.