Back to May 2026 Industry Update

May 2026 Industry Update: Truckload Rates

Main Takeaways

- Average spot rates moved higher in April following a slight dip in March, slightly outpacing gains in the contract market.

- Average fuel prices continued to climb to their highest level in three years and are nearly $2.00 per gallon higher compared to the same time last year.

Summary

Average rates across both the spot and contract markets remained under significant upward pressure in April, driven by elevated fuel prices and tightening capacity conditions. Rapid fluctuations in diesel prices over the past two months have made spot rate movements a less reliable indicator of underlying market conditions, given the typical lag between fuel spikes and spot rate responses. The recent decline in linehaul rates following the nearly $0.30 drop in benchmark retail diesel prices between April 14 and April 28 supports this dynamic.

While carriers operating in the spot market are not directly reimbursed for fuel costs, tighter market conditions and ongoing capacity contraction have improved carriers’ ability to pass through higher diesel prices more quickly. Continued strength in spot pricing, combined with improved cost pass-through, has further incentivized carriers to prioritize spot freight over contractual volumes that were priced under softer market conditions, contributing to additional inflationary pressure on contract rates. Since the start of Q4 last year, average contract rates have increased approximately 6% in a relatively steady fashion, reflecting a meaningful rise in the market value of long-term transportation agreements

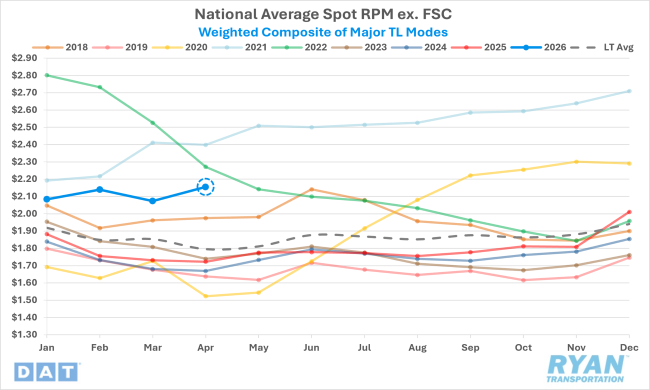

DAT National Average Spot Rates excl. FSC, Weighted Composite Index

Key Points

- After a brief pullback in March that interrupted a three‑month streak of gains, average truckload spot linehaul rates rebounded in April, increasing 4.0% MoM, or just over $0.08.

- On a YoY basis, spot linehaul rates rose 25.1%, marking the widest annual premium since the prior market peak in January 2022.

- All‑in spot rates increased sharply by 6.8% MoM, or approximately $0.18, representing the largest monthly gain since March 2021 and placing rates more than 36% above April 2025 levels.

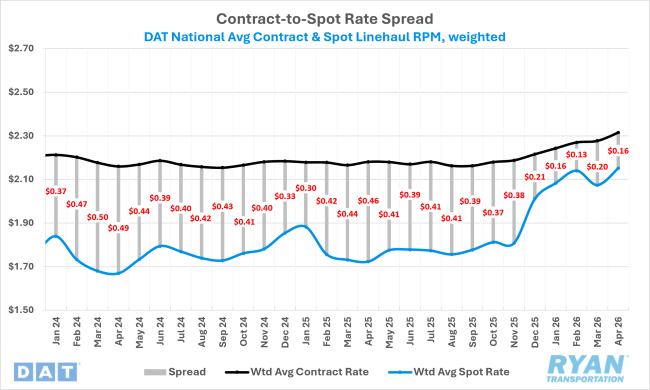

DAT National Average RPM Contract vs. Spot

Key Points

- Initially reported contract linehaul rates increased 2.0% MoM in April, or nearly $0.05, and remained 6.3% higher YoY.

- The contract‑to‑spot rate spread narrowed by $0.04 in April following March’s widening, with contract rates maintaining an approximate 8% premium relative to spot.

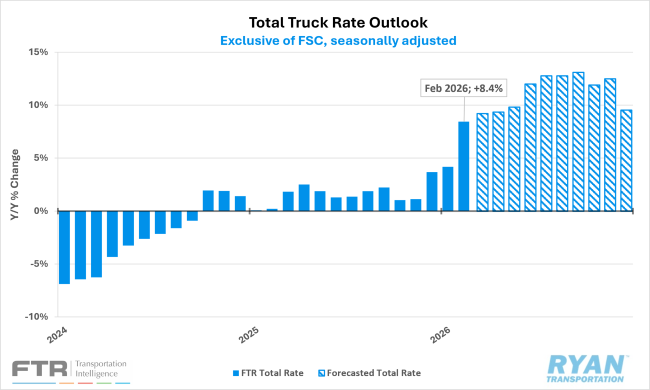

FTR Total Truck Rate & Outlook

Key Points

- FTR revised its 2026 total truckload rate forecast higher in April, projecting +10.4% YoY growth excluding fuel, up from the prior estimate of +9.4%.

- Spot rates continue to drive forecast revisions, with expected growth increased to +19.0% YoY from +17.0%, while contract rate growth was raised more modestly to +6.4% from +5.7%.

- By equipment type, refrigerated and dry van rate growth lead the outlook at +11.6% and +11.3% YoY, respectively, while flatbed rates are expected to increase +9.7%.

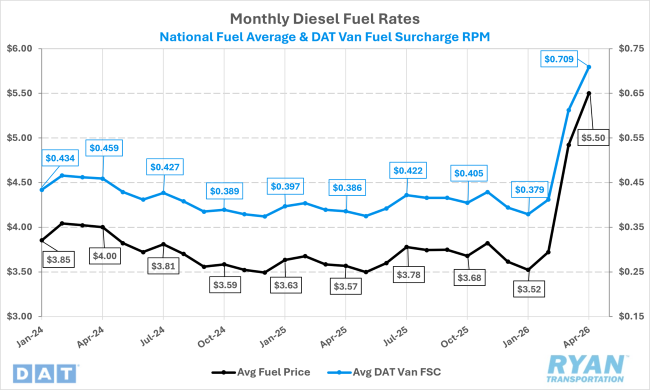

DAT Fuel Trends

Key Points

- The national average monthly diesel price increased $0.58 MoM in April to $5.50 per gallon, its highest level since June 2022, and remained $1.94 per gallon above April 2025 levels.

- According to EIA data, benchmark retail diesel prices peaked at just over $5.64 per gallon on April 6 before declining steadily, ending the month $0.29 lower at $5.35 per gallon.

Outlook

The strong outperformance relative to typical seasonal patterns in April established a significantly higher floor for rates heading into the peak summer shipping season. As capacity tightness persists, the influx of produce, construction-related freight and seasonal beverage volumes are expected to continue putting upward pressure on both spot and contract markets in the near term. However, the magnitude and trajectory of that pressure remain uncertain given the limited visibility surrounding future fuel prices.

This uncertainty is likely to persist as long as the Iran conflict continues, as recent fuel price fluctuations have been driven more by sentiment surrounding potential global supply disruptions than by actual domestic inventory shortages. The sharp pullback in fuel prices during the latter half of April, as optimism increased around a possible diplomatic resolution between the U.S. and Iran, reinforces this dynamic. These reactionary swings will continue to complicate efforts to distinguish how much near-term rate movement is attributable to underlying market fundamentals versus volatility in energy markets.