Back to May 2026 Industry Update

May 2026 Industry Update: Truckload Demand

Main Takeaways

- Overall demand levels remained relatively unchanged compared to March, while annual comparisons have become easier with the Liberation Tariffs going into place this time last year.

- Import volumes have largely normalized and remain below 2025 levels but are still elevated compared to pre-pandemic averages.

Summary

Truckload demand in April changed little from March, as contracted volumes increased modestly MoM while spot market volumes softened. On an annual basis, both spot and contract volumes remained higher, though YoY comparisons have become easier due to the Liberation Day tariffs, which took effect around this time last year. Import volumes continued to normalize following the tariff-driven disruptions of 2025 and provided limited support for domestic freight demand, while the ongoing moderation in imports suggests shippers remain focused on cost control and maintaining leaner inventory levels amid still-elevated warehousing costs.

As has been the case in recent months, overall demand stability is supported primarily by resilience in the manufacturing sector. Meanwhile, early-season produce demand growth has remained concentrated within regional markets — primarily South and Central Florida, Texas, and Southern California — and has yet to noticeably influence national freight demand trends.

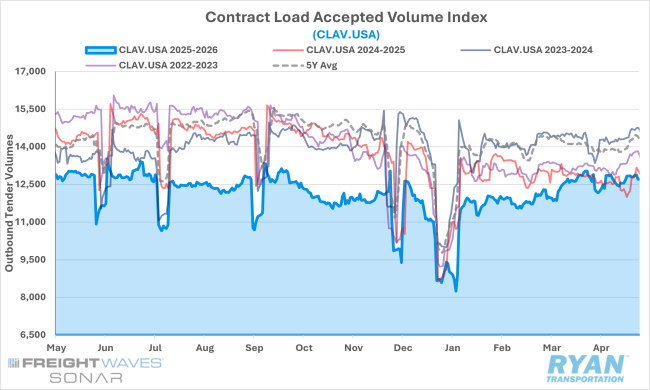

SONAR Contract Load Accepted Volumes Index (CLAV.USA)

Key Points

- Accepted contract volumes increased 1.2% MoM in April, extending a four‑month streak of sequential growth.

- Annual comparisons turned positive for the first time since October 2022, with accepted volumes rising 0.3% YoY compared to April 2025, though they remain approximately 12% lower on a two‑year stacked basis.

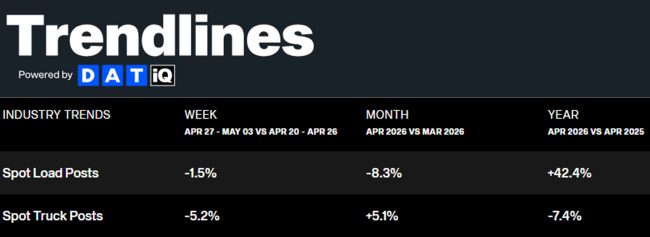

DAT Trendlines

Key Points

- Spot market activity retreated in April following four consecutive months of growth, but continued to outperform year‑ago levels for the fourteenth time in the past fifteen months.

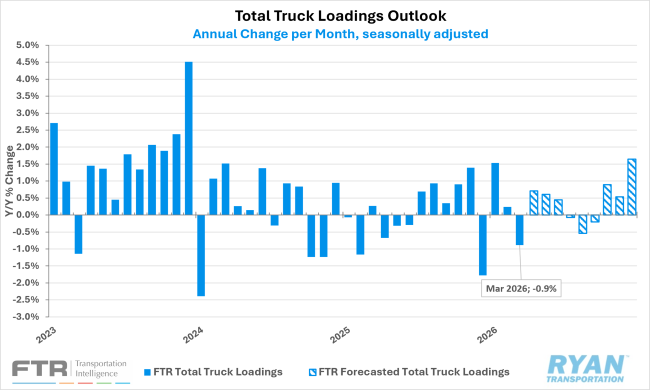

FTR Total Truck Loadings Outlook

Key Points

- FTR revised its 2026 total truckload volume forecast lower, projecting +0.4% YoY growth, down from the prior estimate of +0.8%, largely reflecting weaker expectations in bulk and dump freight.

- Flatbed loadings strengthened materially, with forecast growth revised higher to +3.2% YoY from +1.9%, driven exclusively by building materials demand.

- Dry van loadings were revised modestly lower to +1.3% YoY as softer food volumes offset strengthening automotive and packaged goods shipments.

- Refrigerated loadings expectations eased to +1.7% growth from +2.1%, reflecting slower anticipated growth in temperature‑controlled food and pharmaceutical categories.

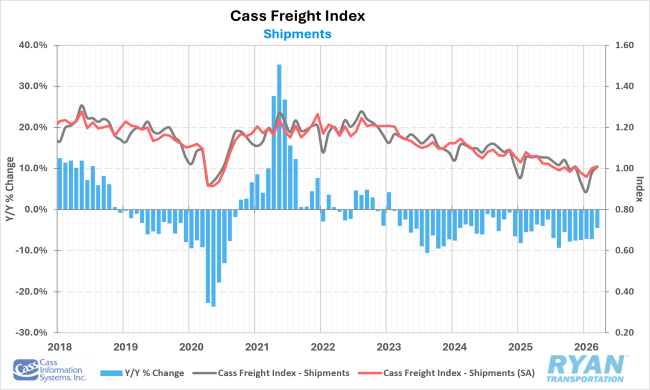

Cass Freight Index Shipments Forecast – February 2026.

Key Points

- Cass Freight Index shipments declined 4.5% YoY in March but increased 3.0% MoM following February’s 10.4% gain.

- Based on seasonally adjusted trends, shipment volumes are projected to rise 1.5% YoY in the second half of 2026, supporting the possibility of a late‑year recovery.

- Near‑term seasonality suggests shipments are expected to decline approximately 5% YoY in April.

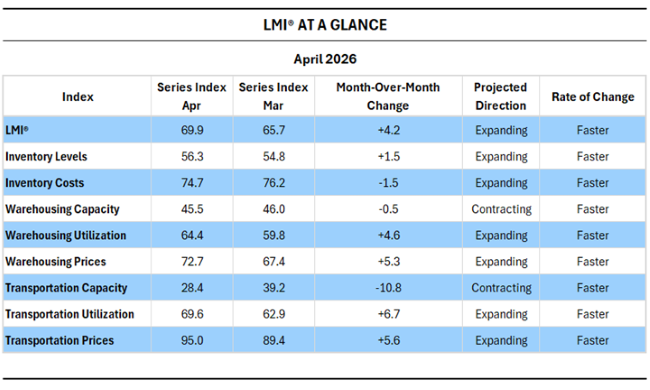

LMI® AT A GLANCE

Key Points

- The LMI® increased 4.2 points in April to 69.9, marking the fastest pace of expansion since March 2022 and exceeding the long‑term average of 61.4.

- Expansion continued to be driven by the freight market, with Transportation Prices reaching their second‑highest reading on record and Transportation Capacity contracting to the second‑lowest.

- Aggregate logistics costs rose to 242.2, a level historically associated with future supply‑driven inflation, contributing to inventory rebuilding as shippers consolidate freight to manage cost exposure.

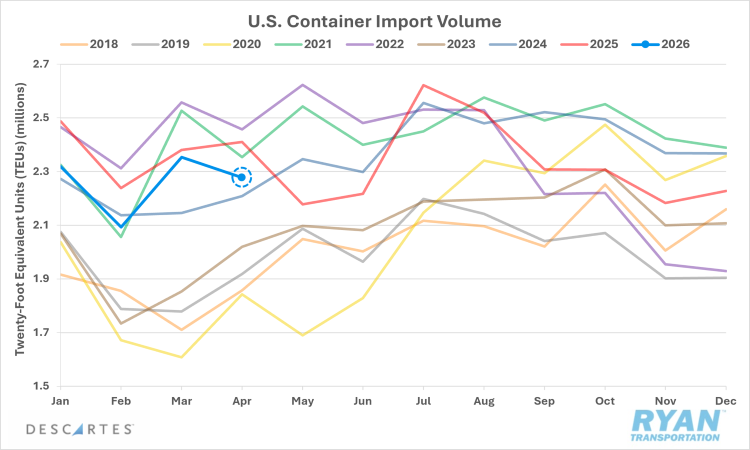

Descartes U.S. Container Import Volumes

Key Points

- U.S. containerized imports declined 3.2% MoM in April to 2.28 million TEUs and 5.5% YoY.

- Despite the pullback, volumes remained 18.7% above April 2019 levels, highlighting continued underlying demand resilience relative to pre‑pandemic norms.

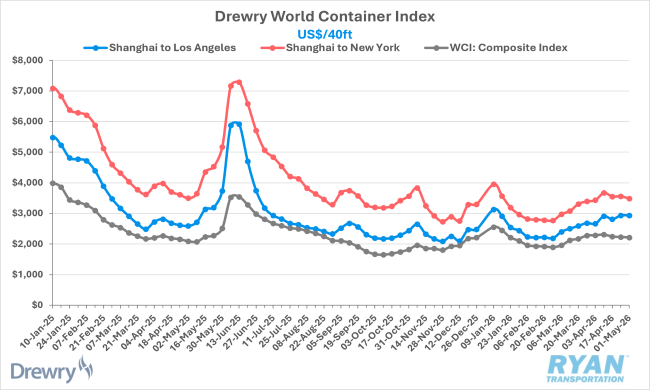

Drewry World Container Index

Key Points

- Global container shipping rates declined steadily throughout April, ending the month 3.1% lower amid weak demand and excess vessel capacity.

- Transpacific rates were mixed, with Shanghai – Los Angeles rates ending April up 10% MoM, while Shanghai–New York rates increased a more modest 1.4%.

Outlook

Heading into the summer shipping season, overall freight demand is expected to strengthen in the near term as produce and beverage volumes increase for refrigerated and dry van carriers, while construction activity continues to support flatbed demand. Spot markets are likely to benefit the most from this influx of freight, as already tight capacity conditions are expected to tighten further with the onset of CVSA International Roadcheck, followed by the Memorial Day shipping push. Longer-term demand expectations remain less certain, however, as sustained elevated fuel prices could create inflationary pressures that weaken consumer demand and constrain future manufacturing output.