Back to March 2026 Industry Update

March 2026 Industry Update: Intermodal

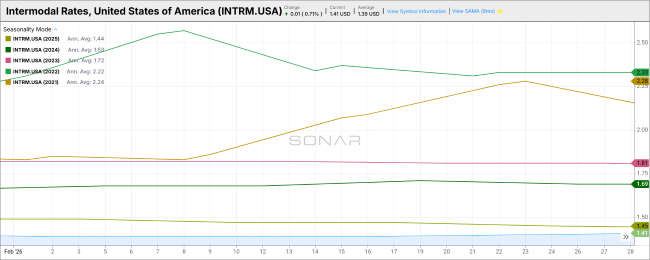

FreightWaves SONAR Intermodal Rates Index (INTRM.USA)

Key Points

- Intermodal spot rates, measured by the FreightWaves SONAR INTRM index, registered no movement in February from January and were $0.04 lower compared to the same month in 2025, suggesting ample capacity remains readily available.

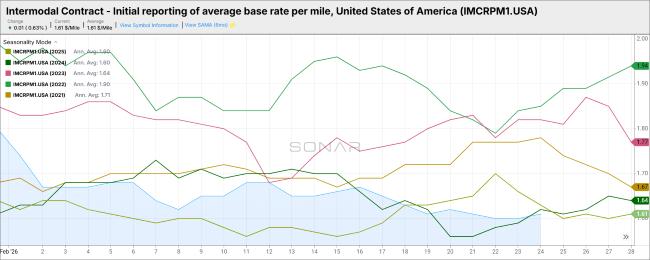

FreightWaves SONAR Initially Reported Average Contract Base RPM (IMCRPM1.USA)

Key Points

- With most new rates established following the latest bid season, initially reported intermodal contract pricing continues to reflect a highly competitive environment, driven largely by abundant available capacity as measured by domestic container supply.

- Commentary from major multimodal carriers in recent earnings calls suggests networks could absorb an additional 15 – 25% in volume, limiting carriers’ ability to push through meaningful rate increases. At the same time, the recent strengthening in the truckload market has not yet fully been reflected in intermodal pricing, though sustained gains in truckload rates are likely to put upward pressure on intermodal contract rates in the near term.

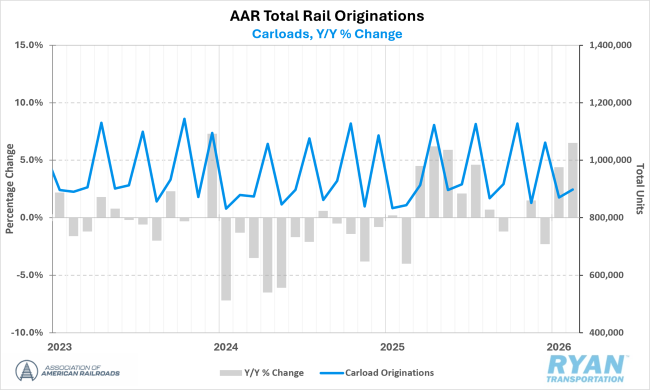

Association of American Railroads (AAR) Total U.S. Rail Carload Volumes

Key Points

- Total U.S. rail carload volumes remained strong in February, rising 6.5% YoY and lifting year-to-date volumes through the first two months of the year 5.5%, or roughly 92,000 units, above the same period in 2025. Growth was broad-based, with 14 of the 20 major AAR-tracked commodity categories expanding, led by industrial-related freight such as coal, chemicals and petroleum products.

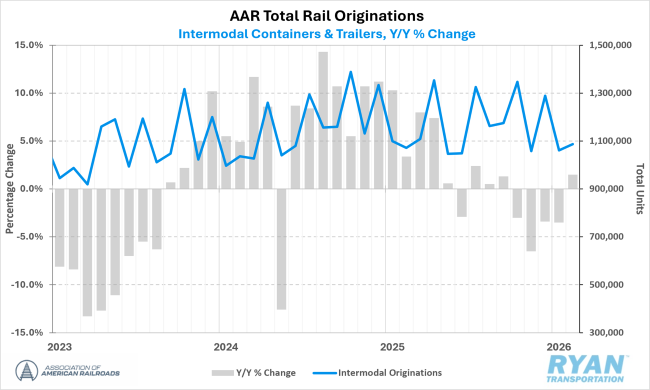

Association of American Railroads (AAR) Total U.S. Rail Intermodal Volumes

Key Points

- Total U.S. rail intermodal shipments also posted solid gains in February, breaking a six-month streak of annual declines. Average weekly intermodal originations rose 1.5% YoY versus February 2025 and reached the highest level ever recorded for the month.