Back to March 2026 Industry Update

March 2026 Industry Update: U.S. Economy

Main Takeaways

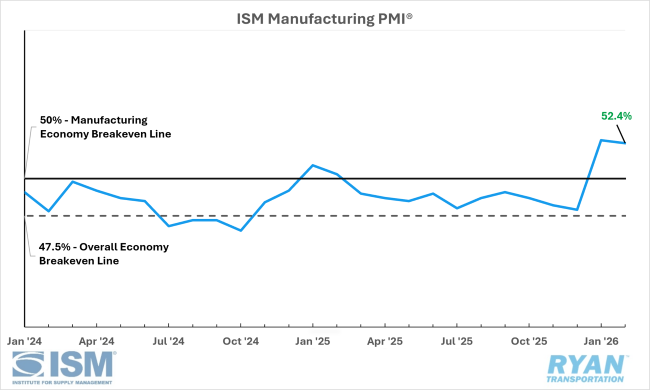

- The ISM® Manufacturing PMI® registered a second consecutive month of expansion in February, driven by continued strength in new orders and production, while prices surged near historic highs.

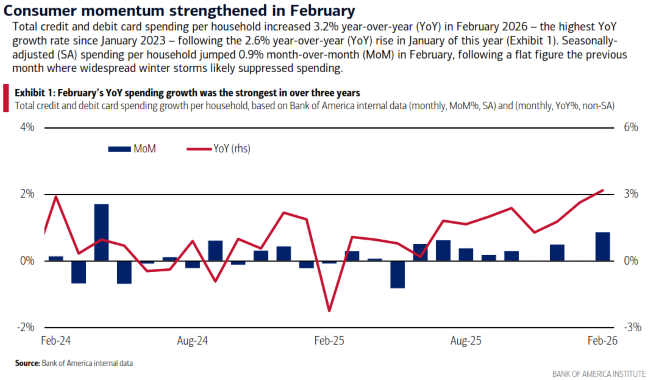

- Consumer spending continued to rise in February, driven primarily by high-income households, while low-income family spending outpaced after-tax wage growth for the first time in nearly four years.

- The growth of the U.S. economy slowed in Q4 2025 due to sharply lower government spending, while consumer spending on services increased and spending on goods declined.

Summary

Ongoing gains in new orders and production kept the U.S. manufacturing sector in expansion territory for a second consecutive month in February, suggesting the potential early stages of a domestic manufacturing recovery. However, persistent weakness in employment, rising input prices and renewed uncertainty surrounding trade policy — particularly as the administration seeks to replace the IEEPA tariffs recently struck down by the Supreme Court — continue to pose risks to the sector’s outlook.

Meanwhile, the first estimate for Q4 2025 U.S. real GDP showed growth slowing to an annualized rate of 1.4% after posting a robust 4.4% expansion in Q3. The deceleration was largely driven by significant drag from government spending tied to the historic 43-day government shutdown, which occurred entirely during the quarter. Consumer spending on services remained the primary driver of growth, followed by private business investment, while spending on goods — particularly durable goods — weakened.

United States ISM Manufacturing PMI

Key Points

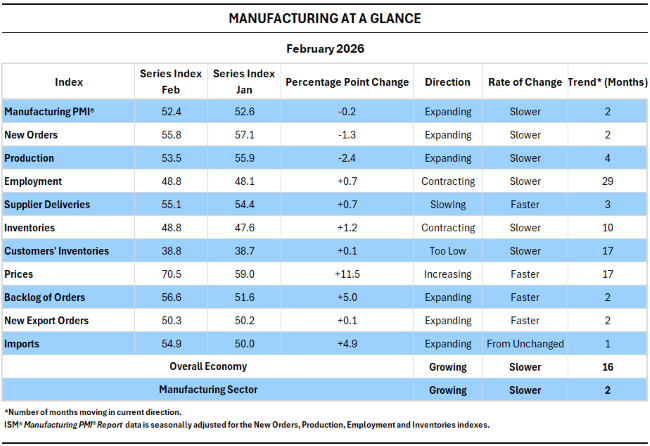

- Domestic manufacturing activity remained in expansion territory for a second consecutive month in February, though growth moderated slightly from January, according to the latest ISM® Manufacturing PMI® Report. The headline PMI® edged down 0.2 percentage points to 52.4%, surpassing consensus expectations and marking only the fourth expansionary reading in the past 40 months.

Manufacturing at a Glance

Key Points

- Of the five primary indexes comprising the ISM® Manufacturing PMI®, two — New Orders and Production — continued to expand but at a slower pace than in January, while the Employment and Inventories indexes remained in contraction territory. Supporting indicators remained constructive, with Customers’ Inventories still in “too low” territory and order backlogs continuing to build. However, price pressures intensified significantly as the Prices Index jumped 11.5 percentage points to 78.5%, its highest reading since June 2022.

Bank of America Consumer Checkpoint, Total Card Spending

Key Points

- Household spending showed strong sequential growth in February, rising 0.9% MoM and 3.2% YoY on a seasonally adjusted basis. Lower-income household spending accelerated to 1.1% YoY from 0.3% in January, while after-tax wage growth slowed to 0.6% YoY, marking the first time since March 2022 that spending outpaced wage growth for this group. Higher-income household spending rose 2.9% YoY as after-tax wage growth improved to 4.2%, while middle-income spending increased 1.7% YoY even as wage growth cooled to 1.2%.

New Residential Construction

Key Points

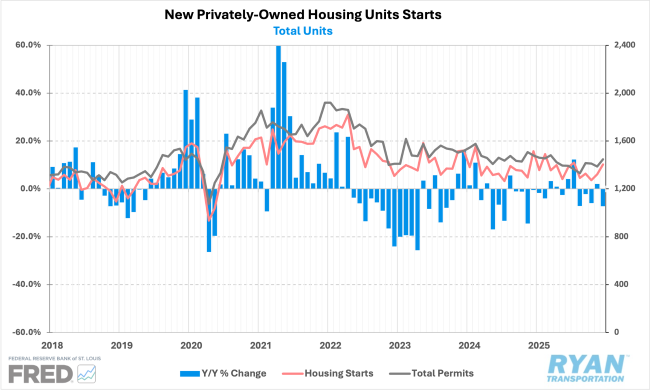

- Despite sequential increases of 3.9% in November and 6.2% in December, total housing starts were down 7.3% YoY in December compared to the same month in 2024. Even so, the preliminary annualized pace of just over 1.4 million starts marked the strongest level since July and exceeded activity recorded in most months throughout 2024 and 2025. Building permits also rose 4.3% MoM in December but remained 2.2% lower YoY, as single-family permits were largely unchanged while multi-family authorizations surged 18.1% MoM and were 18.7% higher than December 2024 levels.

Outlook

Sustained expansion in domestic manufacturing provides favorable support for truckload market recovery and could facilitate freight volume growth amid persistent weakness in housing-related demand. Import activity may provide additional near-term support for truckload demand, as several major trading partners have seen significant reductions in duties following the recent SCOTUS ruling.

Nevertheless, persistent inflationary pressures remain the central concern, as elevated price levels have weighed down consumer spending, particularly on goods, and are expected to accelerate in the coming months, driven by rising energy costs from the recent U.S. military action in Iran. This confluence of inflated prices and the ongoing cooling trend in the labor market has placed the Federal Reserve in a “stagflation” vise, one that may keep interest rates elevated and potentially impede recovery momentum in both the domestic manufacturing and truckload sectors.