Back to June 2026 Industry Update

June 2026 Industry Update: Truckload Supply

Main Takeaways

- Tender rejections rose meaningfully, reflecting tightening capacity and heightened sensitivity to disruptions.

- Employment and equipment data showed mixed signals, with driver payrolls declining but Class 8 orders remaining strong.

- Utilization levels and market indices indicated continued pressure on available capacity across modes.

Summary

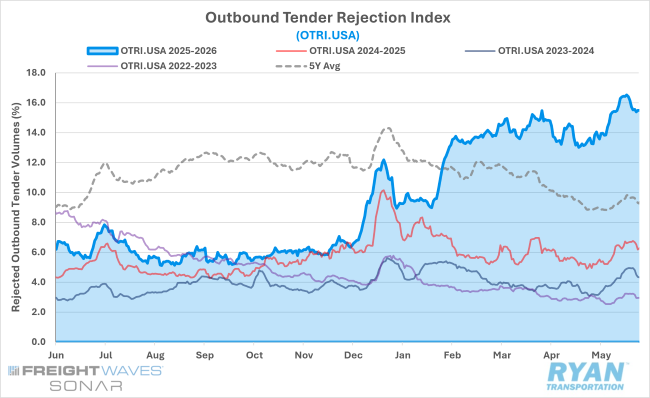

After signs of stabilization late in April and into early May, CVSA Roadcheck week was a good reminder of the truckload markets' ongoing sensitivity to external shocks. While the full results are not expected to be published until late summer/early fall, preliminary estimates reflected a milder inspection period in 2026 compared to 2025, with total inspections dropping from just over 74,000 in 2025 to roughly 69,000 this year. While total violations were down 3.5% YoY, total out-of-service violations rose by just over 1.0%. However, the most notable impact of the 72-hour inspection blitz was a surge in tender rejection rates to their highest levels, above the 15% barrier for the first time since March 2022.

SONAR Outbound Tender Rejection Index (OTRI.USA)

Key Points

- Outbound tender rejections moved higher sequentially in May, after dipping modestly in April, registering 108 basis points higher MoM to just over 15%.

- Rejection rates continued to trend at a premium relative to year-ago levels, with the OTRI averaging roughly 9.1% higher than in May 2025.

- Widespread capacity disruptions brought on by CVSA Roadcheck Week caused OTRI values to spike by nearly 170 basis points, followed by an additional 120 basis point boost during the week leading up to the Memorial Day holiday weekend, pushing rejection rates above 16% and to their highest level since March 2022.

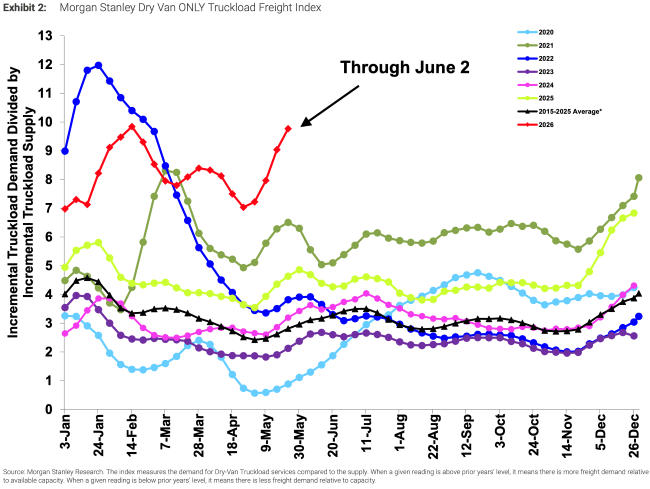

Morgan Stanley Truckload Freight Index

Key Points

- The Morgan Stanley Truckload Freight Index continued its streak of outperformance relative to seasonality in May, driven by ongoing strength in the demand component, while supply-side factors remained in line with historical seasonal patterns.

- Both the reefer and flatbed indices increased sequentially in May, with the reefer performing in line while the flatbed outperformed typical seasonality.

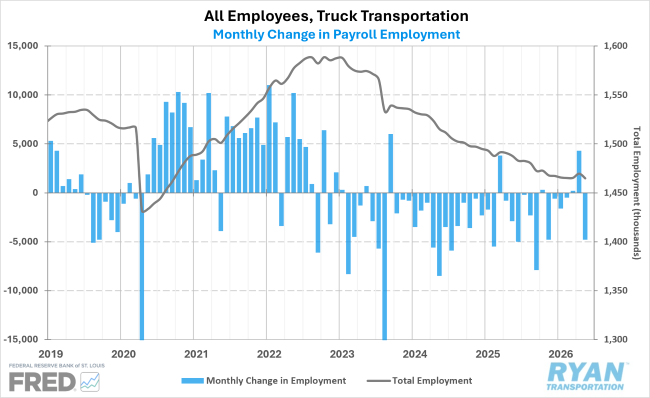

Truck Transportation Payroll Employment

Key Points

- Truck transportation employment declined by 4,400 jobs, seasonally adjusted, in May following downward revisions to March and April estimates totaling 1,400 jobs.

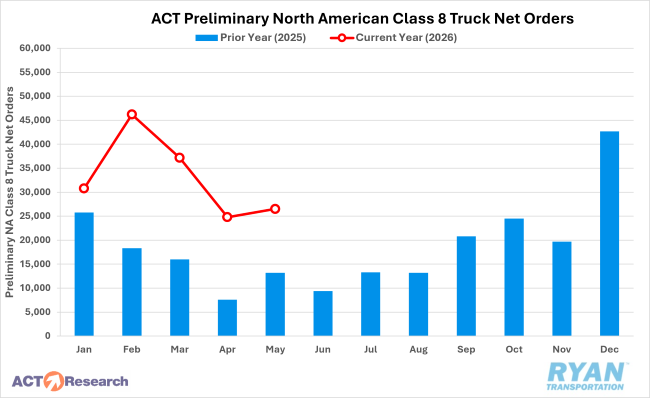

Preliminary North American Class 8 Tractor Net Orders

Key Points

- Improved truckload conditions and increased regulatory clarity further supported equipment demand, as preliminary North American Class 8 truck orders increased sequentially by 4 – 7% MoM, with estimates ranging from 26,500 to 26,600 units, according to ACT Research and FTR.

- On an annual basis, preliminary orders continued to trend well above 2025 levels in May, rising between 100 – 124% YoY despite a limited number of build slots remaining for the 2026 ordering season and entering what is historically a weak seasonal ordering period.

- Ongoing strength in order intake YTD, up 112% YoY, suggests that the remaining build slots for the year are likely to fill or sell out before the end of the order season in August.

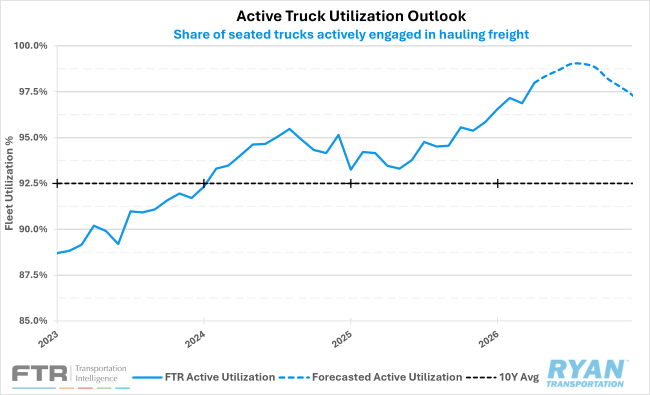

FTR Active Truck Utilization

Key Points

- FTR raised its active truck utilization forecast in its latest update by 1 to 2 percentage points over the next quarter, with utilization now expected to peak at 99% in July and August before moderating heading into 2027.

- The upward revision is based on the considerable disruptions to productivity caused by tight capacity, the recent, unprecedented surge in fuel prices and ongoing enforcement activity targeting foreign truck drivers.

- However, due to ongoing expectations of modest volume growth and concerns of long-term sustainability, active utilization is expected to peak before the fourth quarter, though it is not expected to drop below 96% over the two-year forecast horizon.

Outlook

While heightened enforcement of non-domiciled CDLs and English language proficiency requirements is likely to continue removing capacity from the market, the recent SCOTUS ruling in Montgomery v. Caribe will most likely intensify capacity tightening. In a unanimous 9-0 decision, the Supreme Court held that brokers can now be held liable for accidents that stem from carrier negligence. The impact will force brokerages to sharpen carrier vetting processes and reduce the pool of carriers they are willing to use, disproportionately impacting smaller and newer carriers with limited or questionable safety histories.