Back to June 2026 Industry Update

June 2026 Industry Update: Truckload Rates

Main Takeaways

- Spot and contract rates climbed sharply across equipment types, with several indexes posting their strongest gains in years.

- The spread between contract and spot rates tightened significantly as spot pricing accelerated.

Summary

Average truckload rates surged in May as tighter capacity conditions were further exacerbated by disruptions from CVSA Roadcheck and the Memorial Day holiday. The rate gains observed during the week of CVSA Roadcheck were not just the largest compared to past DOT Safety Weeks but also marked the largest week-over-week increase on record. The continued strength in average spot rates is putting upward pressure on contract rates, resulting in the largest MoM increase in average contract rates since March 2021.

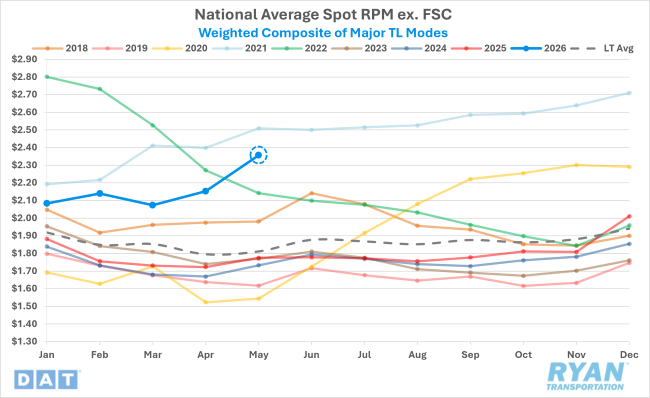

DAT National Average Spot Rates excl. FSC, Weighted Composite Index

Key Points

- After rebounding in April, total truckload spot linehaul rates continued to climb in May, surging by 9.4% MoM ($0.20), just a fraction of a cent behind the December MoM increase, the largest in the past ten years.

- Compared to May 2025, total truckload spot rates excluding fuel were up 32.8% YoY ($0.58) and 29.6% ($0.54) above the long-term average.

- When including fuel, total all-in truckload spot rates rose 7.6% MoM ($0.22) and were 43.8% higher ($0.95) compared to the same month last year.

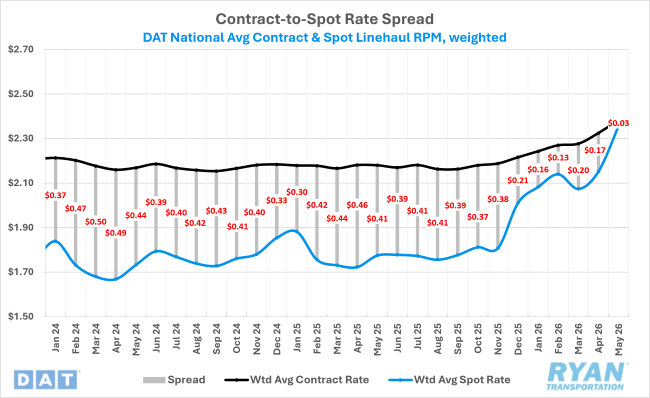

DAT National Average RPM Contract vs. Spot

Key Points

- Initially reported total truckload contract linehaul rates increased 2.8% MoM ($0.07) in May and were up 9.4% YoY ($0.20).

- The sharp increase in spot rates narrowed the contract-to-spot spread to its lowest level since February 2022, with contract rates trending at just 1.1% ($0.03) premium relative to spot rates, down from the 7.6% premium recorded in April.

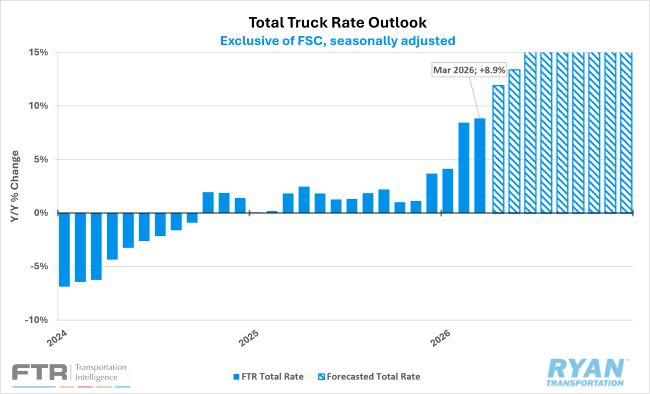

FTR Total Truck Rate & Outlook

Key Points

- FTR’s 2026 forecast for total truckload rates was revised sharply higher in May, rising by 4 points to +14.4% YoY growth, up from the prior estimate of +10.4%.

- The spot rate forecast continued to drive forecast revisions, with rates expected to grow by +28% YoY from the previously reported outlook of +19.0%, while the contract rate outlook improved to +7.9% YoY, up from +6.4% previously.

- By equipment type, upward revisions to flatbed rates were the strongest, with the outlook now projecting +15.2% YoY growth (+9.7% previously), while dry van and reefer forecasts improved to +14.6% and +14.9% YoY, respectively (up from +11.6% and +11.3% previously).

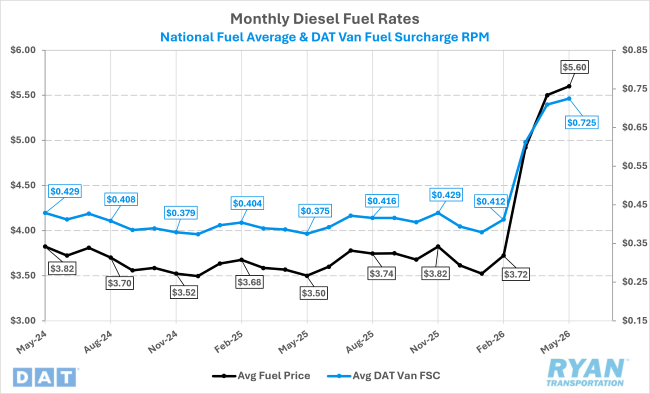

DAT Fuel Trends

Key Points

- The national average monthly diesel price increased just under $0.10 MoM in May to $5.60 per gallon, its highest level since June 2022 and $2.10 per gallon above May 2025 levels.

- Similar to the trend observed in April, benchmark retail diesel prices surged at the start of the month to $5.640 per gallon on May 4 before declining steadily throughout the remainder of the month, ending roughly $0.12 lower at just over $5.52 per gallon.

Outlook

The rate gains over the past two months have established a new floor as the industry progresses through the busy summer shipping season and 100 Days of Summer. Rates are likely to remain elevated off this floor through the rest of Q2 and into Q3. Further volatility and pricing pressures are expected to intensify at the end of June, driven by a culmination of the end-of-month and end-of-quarter push by shippers, followed by the Fourth of July holiday weekend.