Back to April 2026 Industry Update

April 2026 Industry Update: Truckload Rates

Main Takeaways

- Average spot rates hit their highest level in nearly four years, largely attributable to further outsized gains in the flatbed sector.

- The national average price of diesel registered its largest ever monthly gain on record as three of the 11-largest week-to-week increases in diesel prices were reported in March, with the largest of all time, 96 cents a gallon, occurring during the week of March 9.

Summary

Average rates strengthened across both the spot and contract markets in March, though the underlying drivers differed. In the spot market, a sharp increase in fuel prices — rising approximately 40% since the onset of the Iran conflict — contributed meaningfully to rate gains, alongside tightening market conditions that enabled carriers to more readily pass through higher diesel costs to shippers.

Excluding fuel surcharges to isolate underlying rate movement, average spot rates were generally weaker across most truckload segments, with the notable exception of flatbed, which continued to exhibit outsized momentum. Nevertheless, the growth in spot rates and improved ability to immediately pass through volatile fuel prices likely motivated carriers to prioritize spot freight over contractual volumes that were priced in softer market conditions, leading to further upward pressure on contract rates.

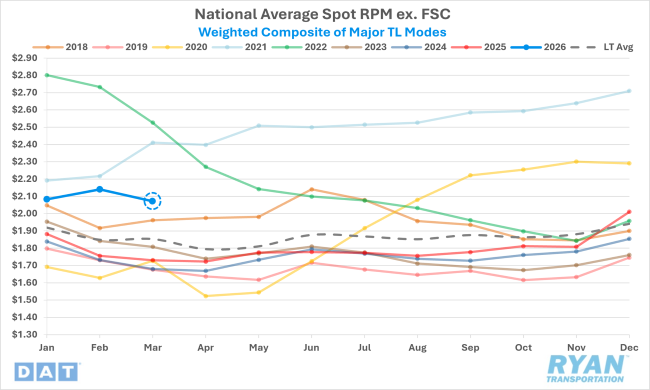

DAT National Average Spot Rates excl. FSC, Weighted Composite Index

Key Points

- Total average linehaul spot rates across all modes eased 3.2% MoM in March after three consecutive months of gains. On an annual basis, spot linehaul rates remained firmly above year‑ago levels, up 19.7% YoY. Although carriers operating in the spot market do not receive fuel surcharges, excluding a calculated surcharge enables analysis of changes in the portion of rates not required to recover fuel costs.

- Accordingly, in contrast to linehaul rates, all-in spot rate movements have been more volatile, with total average spot rates across all modes increasing 5.6% MoM and standing nearly 27% higher than March 2025 levels.

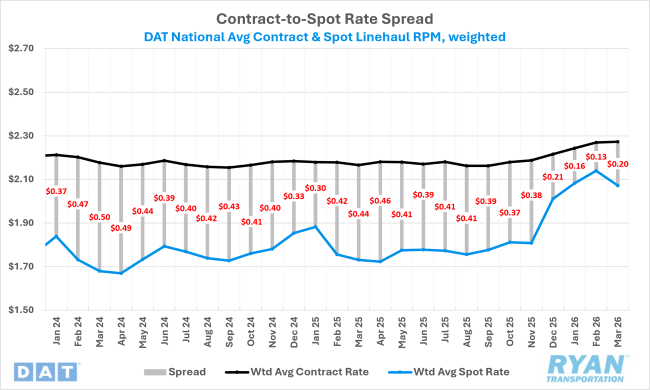

DAT National Average RPM Contract vs. Spot

Key Points

- Initially reported average contract linehaul rates across all modes edged higher by 0.1% MoM in March, following solid gains in January and February, and continued to reflect a 10.7% premium to year‑ago levels.

- After narrowing over the prior four months, stable contract pricing alongside softer spot linehaul rates widened the spread between the two markets, with contract rates trading at roughly a 10% premium to spot — up from a four‑year low of 6.1% in February.

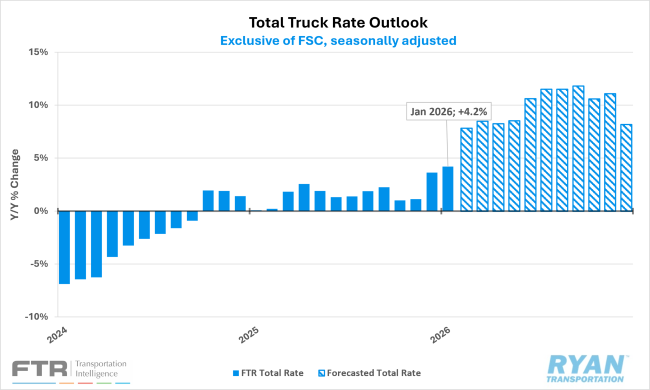

FTR Total Truck Rate & Outlook

Key Points

- FTR Transportation Intelligence revised its 2026 truckload rate forecast higher in its latest monthly market update, projecting total truckload rates to increase 9.4% YoY, excluding fuel, representing a 2.7 percentage point increase from the prior outlook of 6.7% growth.

- Spot rates remain the primary driver of the upward revision, with FTR now forecasting spot rate growth of just over 17% YoY in 2026, up nearly 6 percentage points from the previous projection of 11.5%, while contract rate growth was revised more modestly to 5.7% YoY from 4.7% previously.

- By equipment type, dry van rates saw the largest upward revision, to 10.5% YoY (from 6.8%), followed by reefer at 11.4% (from 9.0%) and flatbed at 7.9% (from 6.0%).

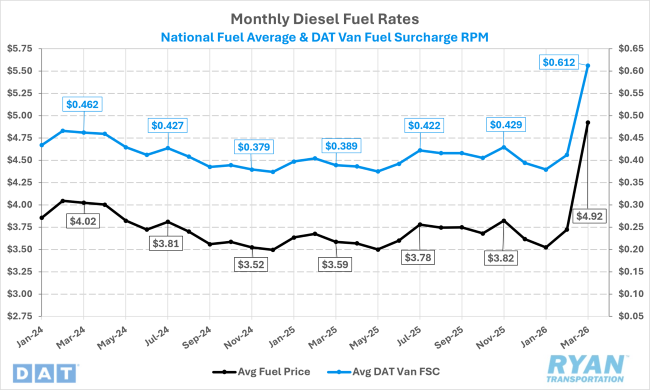

DAT Fuel Trends

Key Points

- Average fuel prices surged in March amid ongoing U.S. military involvement in the Iran conflict and the closure of the Strait of Hormuz, through which roughly one-fifth of global oil supply flows, further disrupting energy markets.

- According to the Energy Information Administration, the monthly average price of diesel increased by nearly $1.20/gal MoM in March — the largest monthly gain since reporting began in 1994 — lifting prices to approximately $1.34/gal above year-ago levels.

- Meanwhile, the agency’s latest Short-Term Energy Outlook projects diesel prices to peak above $5.80/gal in April and average $4.80/gal in 2026, up roughly 40% from its pre-conflict forecast of $3.43/gal.

Outlook

Typical seasonality patterns suggest a modest softening in overall truckload rates in April, followed by a rebound in May and continued firming through the summer months. Nonetheless, persistent capacity tightness combined with ongoing demand growth — particularly as produce and construction-related volumes begin to accelerate — should continue to allow carriers to pass through further increases in diesel prices and sustain upward pressure on both spot and contract pricing in the near term. However, the durability of the current rate environment over the mid- to long-term remains much less certain as prolonged periods of elevated rates generally incentivize capacity to re-enter the market, while a sustained, broad-based demand driver has yet to fully materialize.