Back to April 2026 Industry Update

April 2026 Industry Update: Truckload Demand

Main Takeaways

- Contract volumes rose steadily in March but continue to trend below 2024 and 2025 averages for the month.

- U.S. containerized imports rebounded from February’s decline and remain well above pre-pandemic averages for March.

Summary

Overall freight demand continued to show signs of recovery, as outbound tender volumes trended higher throughout March and briefly surpassed year-ago levels late in the month, for the first time since November 2024. However, this comparison is against a relatively weak prior-year baseline, as early 2025 marked the onset of demand-side softening underpinned by increased trade policy uncertainty, making YoY gains less indicative of underlying strength. Relative to 2024 levels, tender volumes remain in deficit, though the gap has steadily narrowed over the past two months.

Continued strength in industrial activity has been the primary driver of the recent improvement in shipping volumes, as illustrated by notable gains in flatbed demand. Alternatively, the rebound in import activity following the Chinese Lunar New Year, and the leaner inventory strategies companies have adopted to mitigate elevated warehousing costs, contributed additional upward pressure on truckload demand.

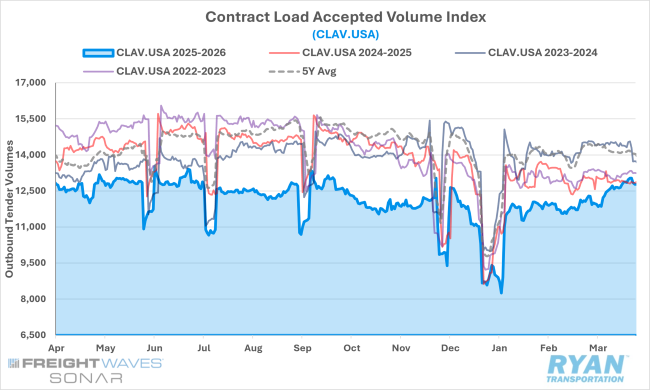

SONAR Contract Load Accepted Volumes Index (CLAV.USA)

Key Points

- Average contract load tenders rose 5.4% MoM in March, extending a third consecutive monthly increase. As a result, year‑over‑year comparisons have tightened to their narrowest spread since November 2024; however, volumes continue to trail March 2025 levels by 3.5% and remain 13.3% lower on a two‑year stacked basis.

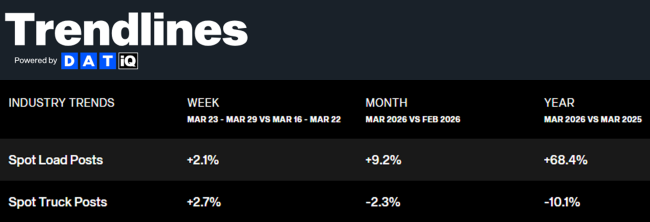

DAT Trendlines

Key Points

- Spot freight gained additional market share in March, as volumes increased sequentially for a fourth straight month and held above year‑ago levels in 13 of the past 14 months.

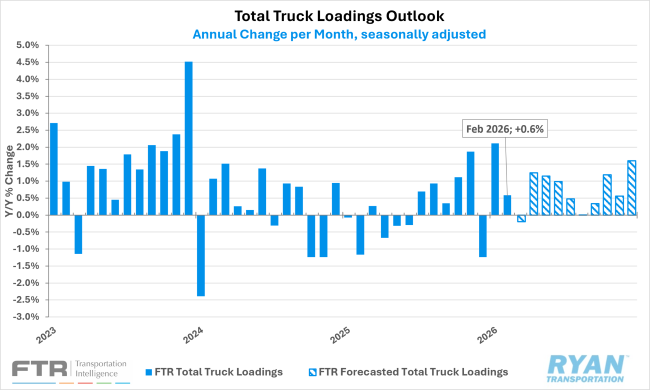

FTR Total Truck Loadings Outlook

Key Points

- FTR Transportation Intelligence modestly revised its 2026 total truckload outlook lower in its latest release, citing weaker growth expectations across bulk aggregates, chemicals and food volumes, with total loadings now projected to increase 0.8% YoY, down from the prior forecast of 1.4%.

- By equipment type, the refrigerated segment saw the most notable downward revision, declining 0.7 percentage points to 2.1% YoY growth, while flatbed and dry van projections were adjusted slightly lower, with flatbed loadings forecast at 1.9% YoY (down from 2.1%) and dry van loadings at 1.4% YoY (down from 1.5%)

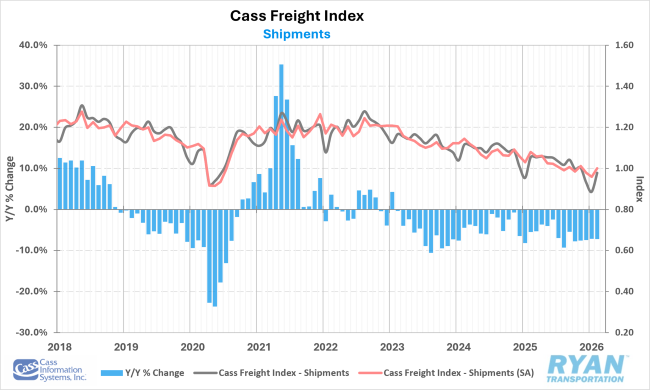

Cass Freight Index Shipments Forecast – February 2026.

Key Points

- The Cass Freight Index shipments component declined 7.1% YoY in February but moved higher by 10.4% MoM from January levels. On a seasonally adjusted basis, shipments rose 4.3% MoM, recovering much of the weather-related disruptions observed in December and January, while the February report noted that typical seasonal patterns suggest further near-term softness, with shipments expected to decline approximately 5% YoY in March.

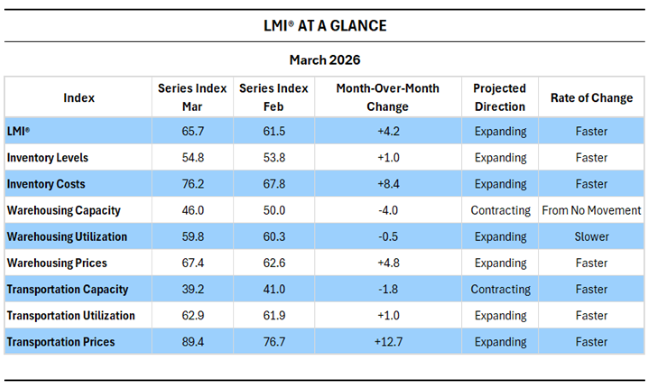

LMI® AT A GLANCE

Key Points

- In its latest reading, the Logistics Managers’ Index increased 4.2 points in March to 65.7, signaling its fastest pace of expansion since May 2022 (67.1).

- According to the report, the acceleration in the headline index primarily reflected continued strength in the freight market, particularly in the transportation components, as Transportation Prices rose to their highest level since March 2022, while Transportation Capacity remained in contraction.

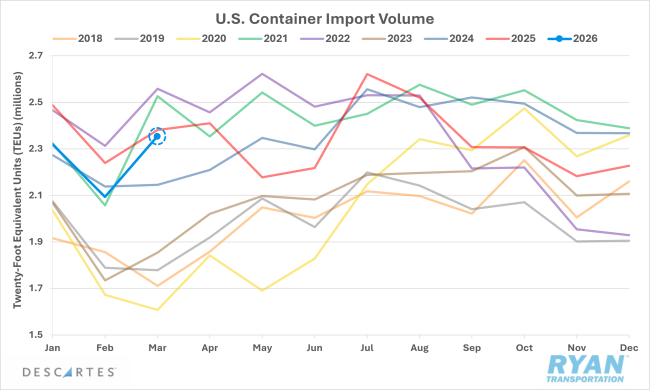

Descartes U.S. Container Import Volumes

Key Points

- U.S. containerized imports rebounded 12.4% MoM in March to 2,353,611 TEUs, though volumes remained 1.1% below year-ago levels.

- According to the Descartes Global Shipping Report, the rebound was consistent with typical seasonal patterns and remained well above pre-pandemic averages for the month, indicating continued resilience in underlying demand despite ongoing policy and economic uncertainty.

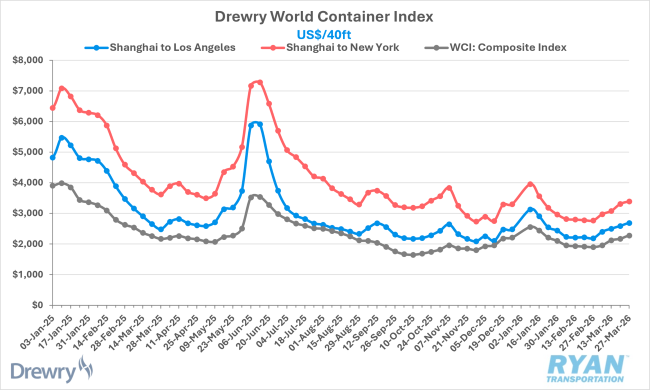

Drewry World Container Index

Key Points

- The Drewry World Container Index — a key benchmark for global container shipping that tracks spot rates for 40-foot containers across eight major trade lanes — rose steadily throughout March, ending the month approximately 20% higher than the final week of February.

- According to Drewry, spot rates on Transpacific routes (Shanghai to New York and Shanghai to Los Angeles) experienced similar increases, stemming from higher fuel costs that prompted carriers to implement emergency bunker fuel surcharges, with rates expected to remain above average in the near term.

Outlook

Near-term shipping activity is expected to continue gaining momentum, as strength in the industrial sector, combined with leaner inventory levels, should support truckload volumes ahead of the peak produce season. Higher tax refunds and potential fiscal stimulus ahead of midterm elections may provide incremental support through consumer spending, while nonresidential construction — particularly data center development — should help drive flatbed demand growth. However, the durability of these tailwinds remains uncertain over the longer term, as macroeconomic risks persist and the potential for shippers’ modal preferences to shift back towards the more cost-competitive rail sector to mitigate exposure to elevated fuel prices, resulting in a net drag on truckload volumes.