Back to April 2026 Industry Update

April 2026 Industry Update: U.S. Economy

Main Takeaways

- Domestic manufacturing activity continued to expand in March, though at a slower rate from February, supported by further growth in production and heightened supply chain pressure, while demand wavered and prices continued to rise.

- Surging gas prices led to sharp gains in household spending in March, with high-income household spending continuing to significantly outpace the other income groups.

Summary

Domestic manufacturing continued to recover, with production levels strengthening and supply chain pressures driving longer lead times. However, uncertainty around the sustainability of this momentum remains, with demand indicators softening amid rising prices and continued weakness in employment. Visibility in the housing market remains limited due to delays in data releases, though prevailing indicators suggest modest improvement alongside ongoing weakness in residential construction and home sales.

In its final estimate for Q4 2025, the Bureau of Economic Analysis revised U.S. real GDP growth down by 0.2 percentage points to an annualized rate of 0.5%, following the stronger 4.4% expansion in Q3. Revisions were relatively minor across major expenditure categories, with consumer spending and business investment remaining the primary contributors to growth, largely offset by declines in government spending associated with the 2025–26 United States federal government shutdown.

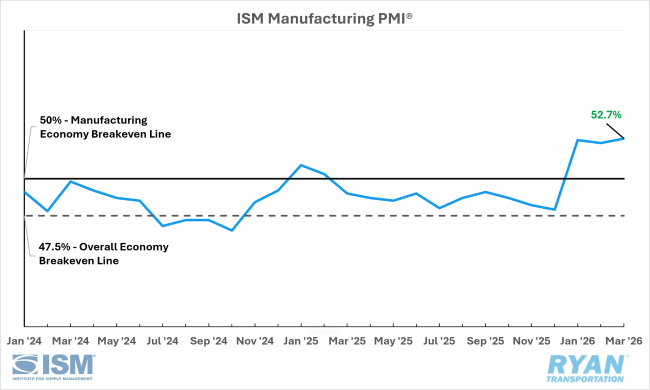

United States ISM Manufacturing PMI

Key Points

- U.S. manufacturing activity expanded for a third consecutive month in March and at a slightly faster pace than in February, according to the latest ISM® Manufacturing PMI® report. The headline PMI® rose 0.3 percentage points to 52.7%, exceeding median expectations of 52.1%.

- Among the six largest manufacturing industries, four — Transportation Equipment, Computer & Electronic Products, Machinery, and Chemical Products — reported expansion, while the share of manufacturing GDP in contraction declined from 21% in February to 16%.

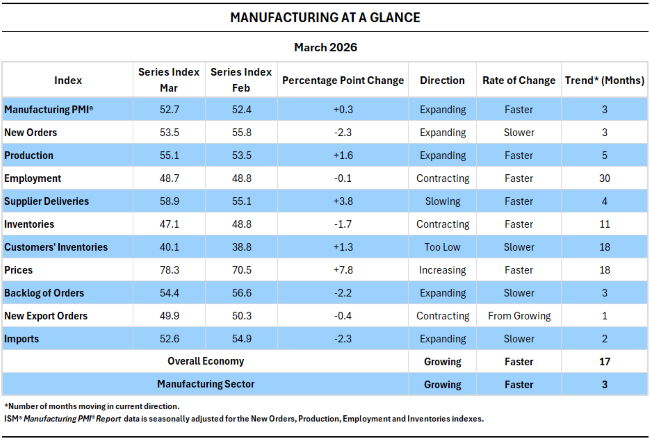

Manufacturing at a Glance

Key Points

- The March increase in the PMI® was primarily driven by two of the five subindexes that directly contribute to the headline figure, with the Production Index continuing to expand at a faster pace as prior months’ orders progressed through the value chain, and the Suppliers Deliveries Index indicating lengthening lead times, consistent with stronger demand or supply disruptions.

- According to the ISM® Manufacturing PMI® report, demand indicators remained mixed, as growth in new orders and order backlogs moderated while new export orders fell into contraction. Meanwhile, both the Employment and Inventories indexes remained in contraction territory while pricing pressures intensified, as reflected in a 7.8 percentage point increase in the Prices Index to its highest level since July 2022.

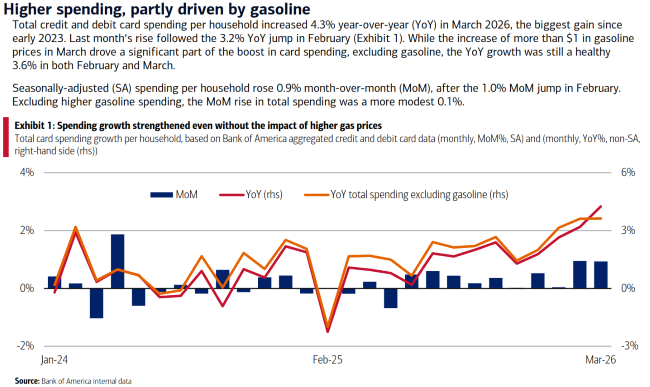

Bank of America Consumer Checkpoint, Total Card Spending

Key Points

- Seasonally adjusted household spending increased 0.9% MoM in March and rose 4.3% YoY, representing the largest annual gain since early 2023. Much of the monthly increase was driven by higher gasoline prices, which led to a 16.5% MoM surge in spending at the pump.

- Spending growth among higher-income households continued to outpace that of other income cohorts, though the gap narrowed modestly in March as gasoline accounted for a larger share of lower-income households' budgets.

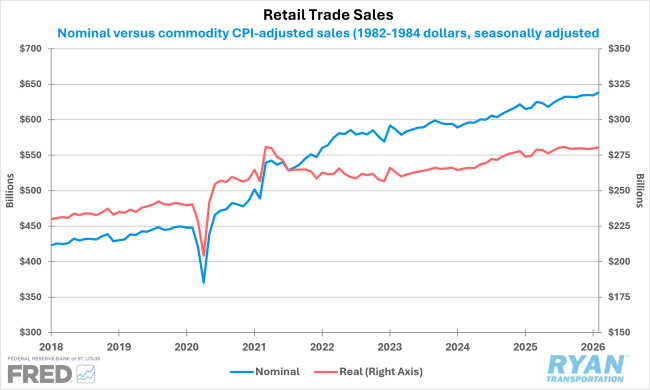

Advanced Retail Trade Sales

Key Points

- Retail and food service sales increased 0.6% MoM in February and were up 3.7% YoY, with all but three retail sectors posting monthly gains and all but four recording annual increases. Retail trade sales, which exclude food services, also rose 0.6% MoM and 3.5% YoY. However, on an inflation-adjusted basis, retail trade sales increased 0.3% MoM and were up just 2.2% YoY compared to February 2025.

Outlook

The Iran conflict and broader geopolitical instability remain the primary sources of uncertainty in the months ahead, as surging oil prices continue to overshadow otherwise improving economic indicators. The resulting inflationary pressure from higher energy costs is likely to weigh on moderating consumer spending and further complicate the Federal Reserve’s path toward additional interest rate cuts, particularly within the current “no hire, no fire” labor market environment.

While policymakers continue to signal the potential for at least one additional rate cut this year, a more cautious stance could emerge if inflationary pressures persist. In that scenario, elevated borrowing costs, combined with rising input and energy prices, may delay capital expenditure decisions and increase the risk that the recent manufacturing recovery loses momentum.